Commonwealth Bank CEO Comyn Overhauls Scandal-Plagued Lender

Commonwealth Bank to Spin Off Wealth, Mortgage Broking Units

(Bloomberg) -- Commonwealth Bank of Australia’s new Chief Executive Officer Matt Comyn has embarked on a massive overhaul of the scandal-plagued lender, announcing plans to spin off its wealth management and mortgage-broking businesses.

The asset management, wealth advisory and Aussie Home Loans units will be placed into a new company known as CFS Group to be listed on the Australian stock exchange, the Sydney-based bank said in a statement Monday. It will also conduct a review of its insurance arm, including a potential sale.

For more detail on the planned spinoff, click here

The move will rid Commonwealth Bank of businesses that have inflicted significant reputational damage and face the prospect of tighter regulation. Wrongdoing in the advice and insurance units -- from allegations that sick customers were denied insurance payouts to planners putting clients into high-risk investments for personal gain -- helped trigger an inquiry into misconduct in the financial industry. Revelations at the hearings have shocked the public and led analysts to downgrade industrywide profit forecasts in anticipation of a tougher future.

“It’s the sensible thing to do,” said Brett Le Mesurier, banking analyst at Shaw & Partners. “The units have caused disproportionate pain for the revenue it generates, have consumed management time and have adversely affected the rest of the business.”

Less than three months into the top job, the restructure shows Comyn is wasting no time in reshaping the nation’s largest lender. Since taking over from Ian Narev in April, Comyn has paid a record A$700 million ($520 million) penalty for systemic breaches of anti-money laundering rules, settled rate-rigging claims, and today appointed six new executives, including a deputy CEO and new chief risk officer.

The split is “another step in our stated priority to become a simpler, better bank,” Comyn said in the statement. “It also responds to continuing shifts in the external environment and community expectations, and addresses the concerns regarding banks owning wealth management businesses.”

The nation’s other big banks are also pulling back from wealth management. Australia & New Zealand Banking Group Ltd. sold its pensions and investment business to IOOF Holdings Ltd. in October, and National Australia Bank Ltd. last month said it would offload its advice, superannuation and asset management units.

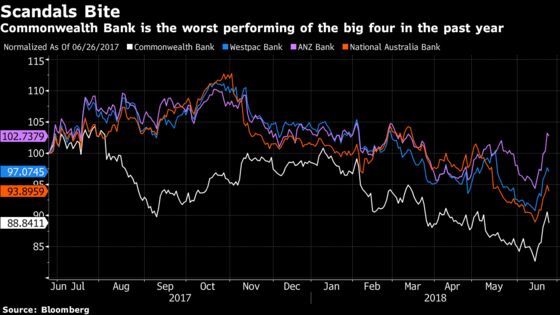

Commonwealth Bank shares declined as much as 2.1 percent in Sydney trading. The stock has fallen 11 percent in the past year, the worst performance among the nation’s four biggest banks.

The new business had net income of more than A$500 million in 2017, Commonwealth Bank said, a fraction of the lender’s annual A$9.88 billion cash profit.

Colonial First State Global Asset Management, which oversees A$207 billion, will be included in the spun-off company, meaning the previously announced initial public offering of the unit will no longer proceed.

To contact the reporter on this story: Emily Cadman in Sydney at ecadman2@bloomberg.net

To contact the editors responsible for this story: Marcus Wright at mwright115@bloomberg.net, Peter Vercoe, Edward Johnson

©2018 Bloomberg L.P.