Shale’s Suffering Indigestion, Not a Heart Attack

Shale’s Suffering Indigestion, Not a Heart Attack

(Bloomberg Opinion) -- The Permian basin is the center of shale’s world, whether it fascinates investors or, as today, repels them. The recent selloff has obscured that.

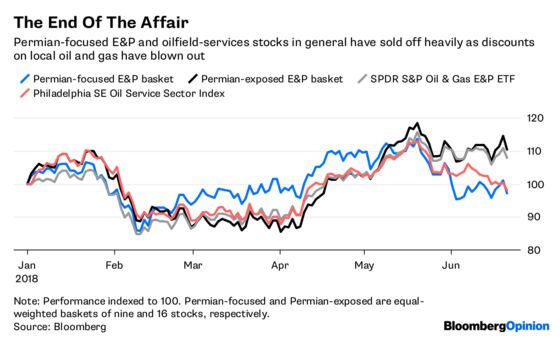

The Permian’s denizens are currently victims of their own success. Production of oil and gas has outrun the pipeline capacity to get it all to market, leading to steep discounts being taken on some of it. Shares of exploration and production firms focused on the basin, and their oilfield services contractors, have tumbled as investors grapple with an uncertain 18 months or so until new pipelines get built (along with all the usual uncertainty about oil and gas).

Notice that stocks with some exposure to the Permian but a few other options too — the “Permian-exposed E&P” crowd like EOG Resources Inc. — have done well. They’re a reasonable place to hide out if you’re still broadly bullish about U.S. oil and think the Permian’s problems are temporary. After all, even as the Permian struggles, other basins like the Bakken are getting some of their mojo back.

By the same token, though, if you think the Permian’s bottlenecks will be largely fixed by the time 2020 rolls around — and not everyone does, it seems — then it might be worth revisiting some of those harsh selloffs. After all, those diversified Permian-exposed stocks are sought-after partly because they’ll still have a stake in the basin when it gets sorted out.

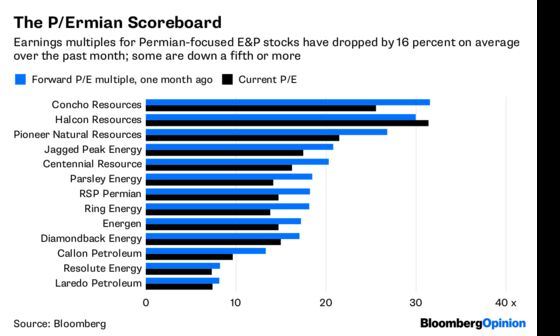

That’s because, when it comes to growth in U.S. oil production, the Permian is still the main event. No one expects it to flat-line even over the next year or two, just grow less quickly. As I wrote here, that disconnect between long-term value and short-term stock gyrations should attract acquirers, be they heavyweights like Exxon Mobil Corp. or just smaller Permian players getting together to sell a scale-and-synergies story.

The latter, if done as all-stock deals, should be a no-brainer (and some activists certainly see it that way). The Permian basin is unusually fragmented, and bigger companies not only get to drill their land more efficiently, they also have the heft to either secure space on existing pipelines or persuade midstream companies to build new ones. Altogether, this should claw back some of that lost ground in valuation:

There’s also a feedback loop to consider here. If the Permian falters more than expected in 2018 and 2019, then that should have a big impact on oil pricing. U.S. production growth is expected to almost match global oil demand this year and cover almost two-thirds of next year’s, the International Energy Agency forecasts. If fewer of those barrels show up for want of a pipe, then that ought to raise prices in general, all else equal (very little can be counted on to remain equal in oil, as this week’s festivities in Vienna demonstrate, but bear with me).

Higher prices would buoy non-Permian E&P stocks and even some of those Permian-focused players with access to exit routes for their oil, such as Pioneer Natural Resources Inc. and Diamondback Energy Inc. This would only serve to widen the gap between the haves and the (generally smaller) have-nots, offering a further impetus for deals.

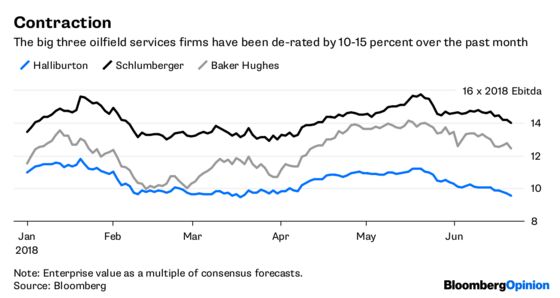

Those higher prices would also help out another set of companies caught in the downdraft, oilfield services contractors.

The services firms have sold off partly because oil prices have come down ahead of the Vienna Group’s meeting. But Halliburton Co. has suffered more, given its higher exposure to U.S. shale basins and fears that frackers in the Permian will take a breather. Less-diversified rivals with an even sharper focus on fracking, such as ProPetro Holding Corp., have taken an even bigger hit.

Concerns about the latter are more understandable, given the number of uncompleted wells in the Permian basin has roughly doubled to more than 3,200 over the past year.

Halliburton, however, has a business spanning not just other shale basins but the whole world. Even if its clients in the Permian ease off, the resulting support lent to the oil price should provide a much-needed push elsewhere in North America and, especially, international fields. Schlumberger Ltd. and Baker Hughes, a GE Co., would stand to benefit even more from an international revival. That said, Schlumberger continues to trade at a sizable premium anyway, and Baker Hughes unfortunately remains in the shadow of the latest Dow Industrials dropout. Plus, of course, Halliburton remains best positioned for when the Permian gets back to full speed.

Don’t mistake the Permian’s indigestion for a heart attack.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

©2018 Bloomberg L.P.