Business Should Brace for the Worst Kind of Brexit

(Bloomberg Opinion) -- When European Union heads meet at the end of this month, they are likely to issue a warning to bureaucracies and firms to step up preparations for a no-deal Brexit, also known as a “hard” or “cliff-edge” Brexit, because that’s where things appear to be heading in the talks between the EU and the U.K.

At this point, it’s calming to view such signals in a game theory context. U.K. Prime Minister Theresa May has an incentive to take things to the edge — possibly beyond October, the current deadline for a deal — so she can get her version of any exit agreement through parliament; she’s more interested in a last-second cliffhanger vote than in a protracted debate. The EU, frustrated by a U.K. side that has nothing to offer, has been talking about the likelihood of a hard Brexit for more than a year, but that could be just a demonstration of willingness to walk away from the table.

If there’s no deal, the U.K. will drop out of the EU in March 2019 without a transition period. That’ll create gaps in regulations and the capacity to enforce them, mainly in the U.K. The FT recently reported that the U.K. government isn’t doing much about that because it doesn’t consider “no deal” a realistic scenario. But believing that the sides are bluffing can result in nasty surprises because the negotiations aren’t exactly poker. It’s a game in which the interests of some of those at the table — at least when it comes to many Conservative Brexiters — are not aligned with those they represent.

It is businesses that really need to prepare for trading across the Channel according to World Trade Organization rules, which mean 2 percent tariffs on most goods but 10 percent on cars and 20 percent on agricultural products. Customs barriers will also spring up, increase costs and slow down deliveries.

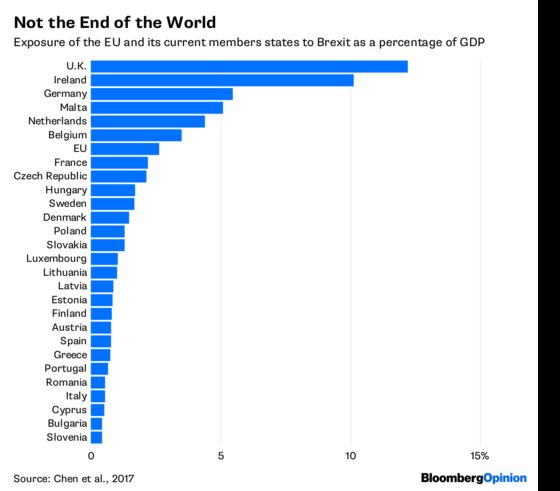

Last year, Wen Chen of the University of Groningen in the Netherlands and his international team of collaborators analyzed which regions in EU countries were most exposed to Brexit. Because of the deep level of the data, this is probably the best analysis of the exposure to date.

Chen’s calculations, however, assume that Brexit will set U.K.-EU trade to zero (there’s no other way to get at the full share of GDP that could potentially be affected). In real life, though, a 2 percent tariff, slightly longer delivery times and the added cost of customs clearance (estimated, for example, at 500 million euros [$578 million] a year for Germany, the EU’s biggest economy) won’t affect trade volumes much. The economic actors who really do need to prepare for a cliff-edge Brexit are primarily in the auto industry, agriculture and finance, where U.K. and European firms would be cut off from operating in each others’ markets directly by the end of passporting.

In the financial services industry, a no-deal Brexit is considered a serious threat. In March, the global Association of Chartered Certified Accountants, whose members work in the entire range of financial companies and banks, published the results of a Brexit-themed survey. Three quarters of its participants work outside the U.K.; 77 percent of those asked said a hard Brexit would be damaging to their business, and 6 percent said their firms would no longer have a viable business model. At the same time, preparations have been going too slowly: 23 percent of the ACCA members (and 31 percent of those working in small firms) said their companies hadn’t even begun planning for Brexit. Only 8 percent said they’d begun to implement their plans, a measly three percentage point increase from March 2016.

That would appear to make the financial services industry a particularly important audience for the upcoming EU warning. A just-released Organization for Economic Cooperation and Development report on the EU downplays the risk — but still notes the potential that a lack of preparedness can cause adverse consequences. “EU entities will probably retain sufficient access to wholesale and retail financial services post-Brexit, as most financial services are currently already provided in the EU-27 and relevant U.K. entities can relocate part of their activities to other EU member states,” the OECD said. “On the other hand, moving from a wholesale banking centered in London to a potentially more fragmented banking landscape might increase the cost of capital for households and non-financial corporations, as the economies of scale and scope of the London industry may diminish.”

It’s somewhat harder for industrial and agricultural firms to Brexit-proof their operations. Finding other markets for products can be a tough task. According to Deloitte, a hard Brexit would cut German car exports to the U.K. by 255,000 a year, worth some 6.7 billion euros or 5 percent of sales. About 18,000 jobs would be endangered. European automakers in total would lose some 8.7 billion euros in sales. Car part sales wouldn’t be hurt as badly because the tariff on them would be 4.5 percent, not 10 percent as for cars, but thousands of jobs could still evaporate as imports from the rest of the world become more economically viable for the U.K.

A survey of German enterprises by the national association of industry and commerce chambers, published earlier this year, showed only 14 percent of firms considered themselves well-prepared for Brexit’s consequences. In particular, the German car industry, the biggest potential loser, is heavily invested in pushing the government and the EU to make a deal. It has assumed too much, and it should focus more on no-deal preparations.

The Irish government and Ireland’s agricultural producers, who stand to lose 39 percent of their exports, worth 4.8 billion euros a year, if the U.K. leaves without a deal, hope for a favorable outcome, too, but at least they’re working visibly to get ready for a cliff-edge Brexit. The Irish Agriculture Ministry has sent special missions to Japan, South Korea, the U.S., Mexico, Saudi Arabia and the United Arab Emirates with a view to shifting some of the exports there. And some firms are already changing their product mix to suit new markets, retooling, for example, to produce Norwegian Jarlsberg cheese for the U.S. and Australia rather than cheddar for the U.K.

Not believing in the possibility of a no-deal outcome could cost businesses billions of dollars in lost revenue. Regardless of whether the U.K. and the EU are only playing a game, it’s a dangerous one. The quality of the players on the U.K. side and the EU’s multitude of other concerns make the worst outcome entirely possible. So all the warnings the parties issue as they try not to blink should be taken extremely seriously.

To contact the editor responsible for this story: Therese Raphael at traphael4@bloomberg.net

©2018 Bloomberg L.P.