Bond Traders Gird for Partial Inversion as Soon as Next Week

Negative slope of the curve has policy makers on edge, with the shape being precursor of recessions.

(Bloomberg) -- The first step in the inversion of the U.S. Treasury curve may be poised to occur as soon as next week.

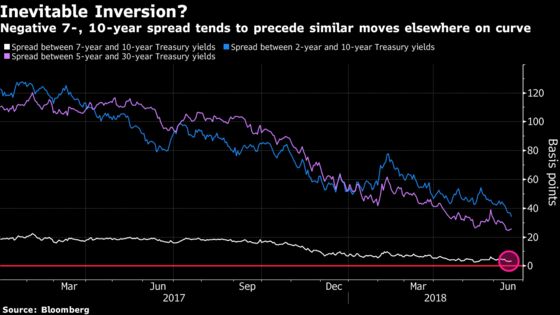

The spread between 7- and 10-year yields slipped below 3.5 basis points Tuesday, after shrinking to 2 basis points last month, the smallest gap since at least 2009. The difference between the maturities, the narrowest among on-the-run benchmarks, may not be particularly well-watched. But its descent into negative territory has historically been a harbinger of similar moves elsewhere along the curve, often in as little as a few days, according to data compiled by Bloomberg and BMO Capital Markets.

Next week’s seven-year auction could lead the notes to underperform just as concerns over trade and global growth anchor longer-term yields, tipping the spread below zero, according to Ian Lyngen at BMO. While hotly traded curve plays including the 2-to-10-year and 5-to-30-year gaps would likely take weeks if not longer to follow suit given current levels, investors will view the initial inversion as a sign of more to come, he said.

“I watch the 7s/10s curve as the proverbial canary in a coal mine,” said Lyngen, BMO’s head of U.S. rates strategy. “Once we see part of the curve dip into an inverted state, then the market will probably be content to let other sectors of the curve invert without as much resistance.”

The shape of the curve has policy makers on edge, given that a negative slope has historically been a precursor of recessions. Several Federal Reserve officials have warned that they should tread lightly with tightening to avoid unintentionally bringing about such an outcome.

Curve Attitude

On Monday, Atlanta Fed President Raphael Bostic said the flattening curve “is not something we can afford to be too cavalier with and think this time is different.” He noted that market perception that the curve is inverting “could trigger its own response that would increase volatility.”

During the Fed’s 1988 tightening cycle, other areas of the curve turned negative around 6 to 28 days after the gap between 7- and 10-year yields went below zero, according to BMO. In the hiking phases that began in 1994 and 2004, inversion took hold even quicker, according to research using a seven-year off-the-run Treasury for modeling periods when the government wasn’t issuing the maturity.

“If the Fed decides to move more this year, I think it’s inevitable that the curve inverts and I think it will be a mistake,” said Colin Robertson, managing director of fixed income at Northern Trust Asset Management. The firm has $423 billion in fixed-income assets under management. He sees greater than a 50 percent chance of the 2- to 10-year spread inverting if the Fed raises rates once more this year, and if the central bank follows its projections and hikes twice more, Robertson sees inversion as a lock.

To contact the reporters on this story: Alexandria Arnold in Seattle at abaca3@bloomberg.net;Liz Capo McCormick in New York at emccormick7@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Boris Korby, Mark Tannenbaum

©2018 Bloomberg L.P.