PetSmart Lenders Square Off as Third Group Forms in Asset Battle

PetSmart Lenders Square Off as Third Group Forms in Asset Battle

(Bloomberg) -- Lender groups across PetSmart Inc.’s capital structure have squared off in groups and enlisted the help of restructuring advisers in an effort to protect their collateral after the company “pulled a J. Crew.”

Certain unsecured bondholders this week became the latest to organize, bringing in law firm Milbank, Tweed, Hadley & McCloy to assist in future discussions with the pet superstore, according to people familiar with the matter.

The Milbank group is one of three that organized and hired counsel after the company transferred over a third of the equity of its Chewy.com unit to separate entities, putting the stake out of reach of some bondholders who financed its purchase a year ago with $2 billion in debt. Lenders brought in the advisers to determine whether certain debt documents permit the transfer of Chewy and if defaults occurred, said the people, asking not to be identified because the discussions are private.

The creditor groups have different goals depending on their holdings, the people said. Lenders lower in the capital structure are pushing for a restructuring deal, one of the people said, while others with more secured holdings are hoping they can regain some of the lost Chewy assets.

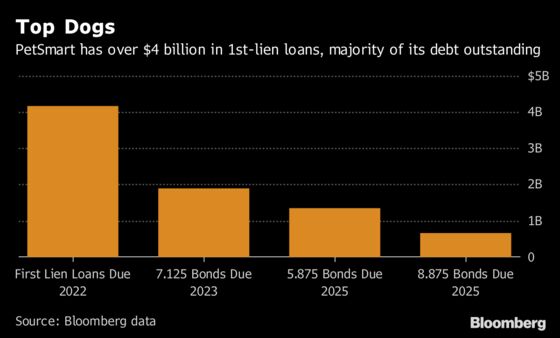

Chewy remains a guarantor of PetSmart’s asset-based loan and a restricted subsidiary under both PetSmart’s credit agreement and senior bonds’ documentation. Strapped with over $8 billion of debt, PetSmart’s next move is highly anticipated by its lenders and the market.

Stake Sale

“Maneuvers to remove Chewy’s guarantee of PetSmart’s bank loans and notes could presage the sale of a minority stake in the company,” said Mark Kaufman, a senior analyst in distressed debt at brokerage firm Ramirez & Co. “It would be a hard sale if Chewy were a guarantor of PetSmart’s debt.”

PetSmart’s secured lenders hired Arnold & Porter Kaye Scholer as legal counsel and FTI Consulting as financial adviser, while a separate group holding both term loan and notes are working with law firm Paul, Weiss, Rifkind, Wharton & Garrison. PetSmart, controlled by private equity firm BC Partners, is working with Kirkland & Ellis as counsel and Houlihan Lokey as financial adviser.

Representatives for Milbank and Houlihan declined to comment. Representatives for Arnold & Porter, Paul Weiss, Kirkland, FTI and Phoenix-based PetSmart didn’t immediately return requests for comment.

J. Crew, Claire’s

PetSmart’s move mimics asset transfers initiated by other distressed retailers, especially those owned by private equity sponsors. J. Crew Group Inc. and Claire’s Stores Inc. have created subsidiaries to hold assets including intellectual property, insulating them from creditors while freeing them up for use as collateral to back new debts.

In its attempt to quell lenders concerns, PetSmart earlier this week shared documents with certain secured lenders that provided supplemental data and pegged the value of Chewy at $4.45 billion. PetSmart’s assessment of Chewy came in response to a letter from counsel for Citigroup Inc., the administrative agent for PetSmart’s term loan, which had requested further information on the Chewy transfer.

Some market participants were anticipating a higher valuation, between $6 billion and $7 billion, two of the people said. The $4.45 billion number, exclusive of cash on Chewy’s balance sheet, was only disclosed to certain secured lenders with access to the memo posted on the private data site.

‘Good Faith’

Based on the language in PetSmart’s debt indenture, it would be "extremely difficult" for bondholders to challenge the company’s $4.45 billion valuation of Chewy, Scott Josefsberg of Covenant Review said in an interview. The company was required to act in ”good faith” to determine the fair market value, he said. Absent of allegations that they didn’t act in this way, "they have a hard time disputing the value."

Chewy, which has yet to turn a profit, saw an improvement in a measure of earnings during its most reporting period. For the first quarter of 2018, the company reported $764 million in sales from Chewy, compared with $650 million in the fourth quarter of 2017. Management has said in the past that Chewy is taking market share from competitors, but that its margins were slimmer than PetSmart’s physical stores.

PetSmart’s term loan due 2022 was quoted at 82.75 to 83.5 cents on the dollar on Friday afternoon in New York, down from 83.5 to 84.25 on Wednesday, according to a person familiar. The company’s 8.875 percent senior traded at 62.75 cents on the dollar, according to Trace bond-price data.

--With assistance from Eliza Ronalds-Hannon.

To contact the reporter on this story: Katherine Doherty in New York at kdoherty23@bloomberg.net

To contact the editors responsible for this story: Rick Green at rgreen18@bloomberg.net, Kenneth Pringle, Nikolaj Gammeltoft

©2018 Bloomberg L.P.