(Bloomberg Opinion) -- Like father, like son.

The Cheung Kong empire’s first deal since founder Li Ka-shing handed over to Victor Li in March is a chip off the old block. The proposed A$11-a-share takeover of Australian gas pipeline operator APA Group Ltd., at an enterprise value of A$22 billion ($17 billion), feels like an almost direct replay of its last mega-purchase, of electric and gas utility Duet Group.

Developed, preferably English-speaking economy? Check. Monopolistic utility asset? Check. Stapled-security structure to minimize tax payments? Check. Punchy valuation? Check.

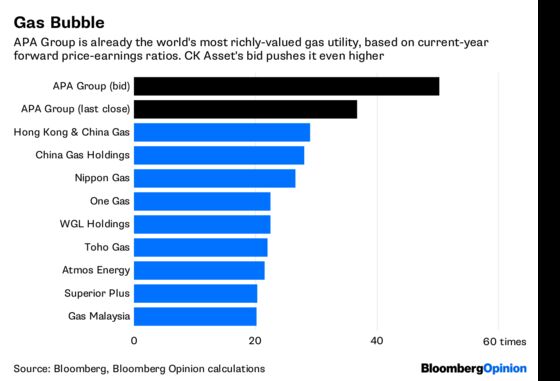

About that valuation. Thanks to its near-monopoly of Australia’s domestic transmission pipes, APA is already the most richly rated gas utility in the world on some measures, with a current-year forward price-earnings ratio of 37 which the current offer lifts to a blistering 50 times. That’s about three times the 16.9 median multiple among 60 companies for which Bloomberg has data, and leaves the teens-to-twenties likes of Facebook Inc., Apple Inc., Alphabet Inc. and Microsoft Corp. in the dust. APA shares jumped 21 percent to A$10.29 in Sydney, ending below the bid.

Can that sort of price be justified? Well, looked at another way it makes perfect sense. For one thing, in enterprise value-to-Ebitda terms it’s only a 15 times multiple, less than Hong Kong & China Gas Co. and China Gas Holdings Ltd., two other Hong Kong-listed gas utilities.

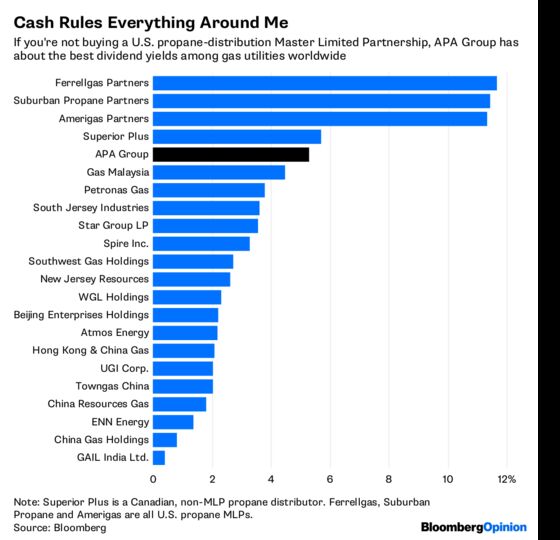

For another, the guiding principle of the Cheung Kong group these days isn’t earnings growth but the mantra of “stable recurring income” – preserving the value of the house that Li Ka-shing built for future generations. On that front, APA is a clear fit. While its price-earnings ratio is high, its 5.3 percent dividend yield is generous, too – barring a handful of North American propane distributors, the highest for a large gas utility anywhere in the world.

The bidders appear to have done their homework. The Cheung Kong consortium, which includes family vehicles CK Asset Holdings Ltd., CK Infrastructure Holdings Ltd. and Power Assets Holdings Ltd., has already had talks with Australia’s foreign investment and antitrust regulators.

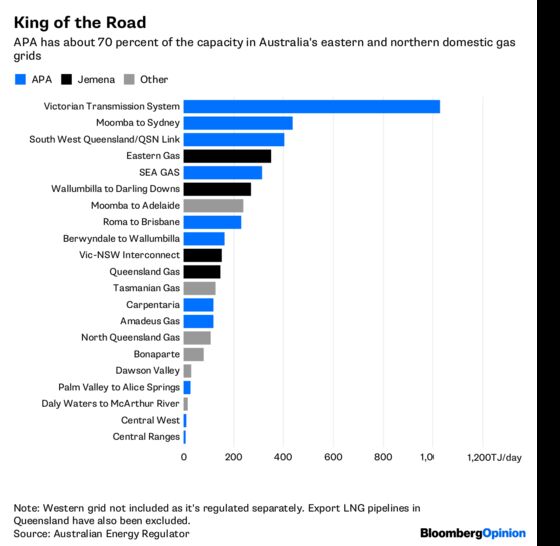

As a result, it’s proposing to divest two pipelines and a gas storage facility and promised a standalone management team to minimize conflicts of interest. The move would largely remove it from Western Australia’s gas grid while maintaining its roughly 70 percent share of pipeline capacity in the north and east of the country.

That would still leave some potential conflicts. CK Infrastructure is among APA's biggest customers, with about 45 percent of distribution customers in the eastern Australian gas grid that's supplied by APA's transmission pipes. Rivals, such as State Grid Corp. of China-controlled Jemena, might not be happy with that arrangement. Still, the fact that a divestment strategy is already in place suggests the bidders are confident they can answer antitrust concerns.

Foreign investment review may be more of a challenge, given Australia’s recent paranoia around Chinese investment and more justified concerns around political influence-peddling and interference with its overseas-Chinese population.

That risk is probably overblown, however. While CK Infrastructure was blocked from buying a government-owned electricity distributor around Sydney in 2016 alongside Beijing-owned State Grid, Li’s successful bid for Duet a few months later indicated that for the moment Australia’s authorities don’t quite consider Hong Kong to be equivalent with China.

As we argued today in relation to China’s proposal to build a national pipeline champion, such assets can be natural monopolies. With such a high fixed cost involved in building the infrastructure and such an infinitesimal marginal cost in moving a cubic meter of gas along an existing pipe, the barrier to potential competitors is all but insurmountable except in situations where demand is growing very rapidly.

That makes APA Group a potent prize for a family dynasty with an eye to the long term. Li Ka-shing may have retired, but his spirit is still strong in the empire he built.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

©2018 Bloomberg L.P.