Oil Rises for Third Day After Surprise Drop in U.S. Inventories

Oil Falls as Traders Worried Over OPEC Assess Growing Stockpiles

(Bloomberg) -- Oil rose for a third day after a U.S. government report showed tumbling domestic crude and fuel inventories.

Futures in New York reversed an early-session decline on Wednesday after the Energy Information Administration said U.S. oil stockpiles declined by 4.14 million barrels last week, the most since March. Before the tally, prices were under pressure as Russia and Saudi Arabia signaled a desire to unwind historic output limits.

“We saw a bit of a reversal after the inventory numbers came out,” said Gene McGillian, market research manager at Tradition Energy. “Instead of an across the board build like we expected, we got the complete opposite of that.”

Oil has retreated from the highs of May after the Saudi kingdom and Russia indicated they supply increases may be needed to counter losses from other producers such as Venezuela. U.S. President Donald Trump on Wednesday reiterated criticism of OPEC for restraining supplies.

The Organization of Petroleum Exporting Countries and allied producers are scheduled to meet meet next week in Vienna. Iraq, Iran and Venezuela have already lodged objections to the Saudi-Russian appeal to relax production caps.

“With everything coming out of OPEC, talk about how many barrels will come back into the market and from whom, there’s just a lot of rhetoric. And until we get to the OPEC meeting, I think trading will be very choppy,” said Tariq Zahir, a commodity fund manager at Tyche Capital Advisors LLC.

West Texas Intermediate crude for July delivery rose 28 cents to settle at $66.64 a barrel on the New York Mercantile Exchange.

Brent futures for August settlement rose 86 cents to $76.74 on the London-based ICE Futures Europe exchange. The global benchmark crude settled at a $10.22 premium to WTI for the same month.

Ending Curbs

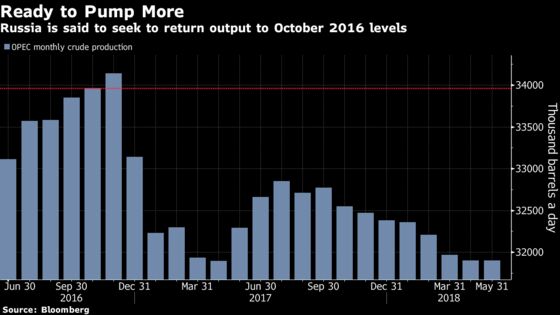

Russia plans to propose the producers’ group proportionally share out a 1.8 million-barrel-a-day increase to their output limit starting as soon as July, said a person with knowledge of the matter. That would effectively end the cuts for any country that has the ability to pump more crude, going further than the previous suggestion for boosting output.

Given the backing of the two largest producers participating in the accord, a supply increase “looks inevitable,” Citigroup Inc. analyst Ed Morse said in a report on Tuesday.

In the U.S., the decline in crude stockpiles was steeper than 11 of the 12 estimates from analysts in a Bloomberg survey. It also ran counter to an industry report a day earlier showing an increase.

Gasoline stockpiles fell 2.27 million barrels and distillate sank by 2.1 million, according to the EIA. That helped push gasoline futures for July delivery up by 1.7 percent to $2.1252 a gallon and diesel up 1.1 percent to $2.1851.

Other oil-market news:

- Investors are waiting for the first dominoes to fall in the Permian Basin as filled-to-capacity pipelines and wavering oil prices pressure drillers to cut back.

- President Trump tweeted about oil prices again on Wednesday, saying: “Oil prices are too high, OPEC is at it again. Not good!”

- A Bloomberg survey showed OPEC will probably overcome internal disputes to agree on a production increase next week.

--With assistance from Tsuyoshi Inajima, Sharon Cho and Grant Smith.

To contact the reporter on this story: Catherine Ngai in New York at cngai16@bloomberg.net

To contact the editors responsible for this story: Reg Gale at rgale5@bloomberg.net, Joe Carroll, Mike Jeffers

©2018 Bloomberg L.P.