Bond Traders Brace for Major Moves in Aftermath of FOMC

Bond Traders Brace for Major Moves in Aftermath of Fed Meeting

(Bloomberg) -- For a Federal Reserve meeting where a rate hike is seen as a given, the stakes are still huge for bond traders heading into Wednesday’s decision.

Investors have piled into front-end wagers and curve plays betting on the timing and pace of rate increases in the second half of the year and beyond. That leaves plenty of room for market moves depending on what Fed officials signal in a few key areas. Namely, their updated dot-plot projections and a potential change to the rate paid on excess reserves.

“The importance of this meeting is to get a clear picture of the what-if scenarios for 2018, as there are a lot of balls up in the air,” said Todd Colvin, senior vice president at futures and options broker Ambrosino Brothers in Chicago.

Here are the corners of the market poised for the biggest post-Fed reactions.

20 Versus 25

After May’s Federal Open Market Committee minutes suggested that officials might only raise the interest on excess reserves (IOER) rate by 20 basis points at an upcoming meeting, volumes across fed funds and eurodollar futures spiked as implied rates tumbled. After retracing somewhat, the July contract is now printing about 22 basis points above the fed effective rate of 1.70 percent. That suggests traders see about an 80 percent chance of the Fed opting for the smaller IOER increase, according to John Brady, a managing director at R.J. O’Brien & Associates in Chicago.

If officials do tinker with the IOER rate this week, traders will also look to Fed Chairman Jerome Powell’s press conference for hints as to whether policy makers intend to use that approach again, or if this time would just be a one-off.

Three Versus Four

If traders are wagering on any change in the FOMC’s’ median projection for tightening this year, there’s a good chance they’re doing it using the January 2019 fed funds futures contract. It’s currently trading at 97.735, or an implied rate of 2.265 percent. That puts it squarely between three and four hikes by year-end.

Should officials’ updated dot plot forecasts show them leaning toward four hikes for the year, up from the three they flagged in March, the contract should see an immediate repricing as the market brings its expectations more in line with the Fed’s. And if the dot plot stays at three hikes for 2018? Look for the January 2019 fed funds contract to rally.

In the cash market, the shape of the yield curve is riding on the meeting’s outcome too.

After a mid-May pause, the flattening that dominated the Treasuries market for months has roared back, sending the gap between two- and 10-year yields toward 40 basis points once again. Tom di Galoma, managing director of government trading and strategy at Seaport Global Holdings, is among those favoring flatteners heading into the Fed decision. He says it’s likely the Fed will signal rates hikes for both September and December.

That view has been gaining traction in the markets even as some policy makers have warned that the threat of an inverted curve may cause the Fed to dial back its tightening plans.

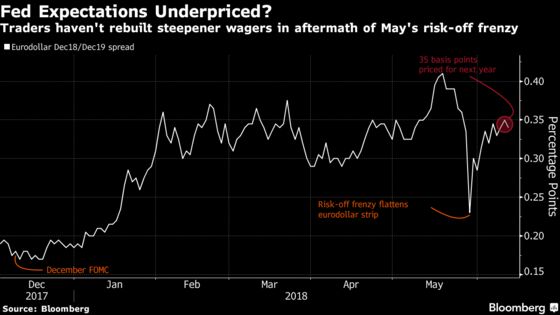

Beyond 2018

Traders continue to be stubbornly dovish on the pace of rate increases beyond 2018 relative to policy makers’ projections. With the spread between December 2018 and 2019 eurodollar contracts now at about 36 basis points, traders are pricing in roughly one-and-a-half hikes next year, should FRA-OIS remain stable. That compares to the three that policy makers are signaling in the dot plot.

If firming inflation and near-record low unemployment prompt officials to forecast a steeper path of hikes down the line -- just as they did in March -- traders would be in store for a major shakeout.

To contact the reporters on this story: Alexandra Harris in New York at aharris48@bloomberg.net;Edward Bolingbroke in New York at ebolingbrok1@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Boris Korby, Mark Tannenbaum

©2018 Bloomberg L.P.