Trans Mountain Seen Drawing Pension Funds or Returning to Kinder

Trans Mountain Seen Drawing Pension Funds or Returning to Kinder

(Bloomberg) -- So now Justin Trudeau owns a pipeline. Who will take it off his hands remains an open question.

Canada said Tuesday it would buy Kinder Morgan Inc.’s Trans Mountain pipeline, with its expansion project and shipping terminal, for $3.5 billion before eventually selling the project to a new buyer. Finance Minister Bill Morneau, speaking Tuesday in Ottawa, said it was too soon to say if Canada would sell in the short or medium term, but didn’t want to hold the project in the long term.

Finding a buyer for Trans Mountain could be tricky amid ardent opposition from British Columbia, the Pacific Coast province it crosses, along with environmental and some indigenous groups. That opposition was enough to make Kinder throw up its hands and halt construction last month. Even as Morneau struck an upbeat tone on the potential pool of buyers, he didn’t give a specific time frame for a deal.

“Many investors have already expressed interest in the project, including Indigenous groups, Canadian pension funds, and others,” he said.

One analyst floated another potential home: Kinder Morgan itself.

Canada’s purchase may “‘be a vehicle to indemnify the project against regulatory risk,” Katie Bays, an analyst with Height Securities LLC in Washington, said in a telephone interview. “Once the construction is complete or once regulatory risk evaporates, whichever comes first, the project could be repurchased by Kinder Morgan.”

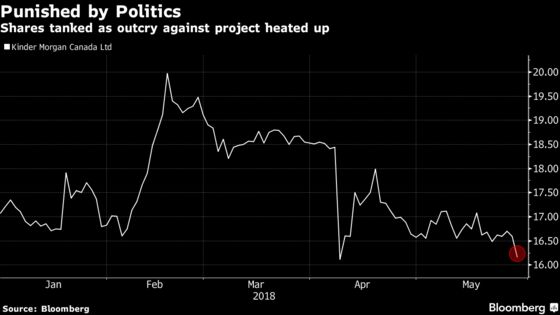

Kinder Morgan Canada, the unit that raised C$1.75 billion ($1.3 billion) for the project in an initial public offering last year, declined to comment on the speculation.

Private Equity

If Kinder doesn’t want it back, some investors have shown interest in the project in the past.

Before deciding on taking the Canadian unit public, Houston-based Kinder Morgan ran a dual-track process that also entailed exploring a joint venture of the pipeline project. That possibility attracted interest from U.S. private equity firm ArcLight Capital Partners and Australia’s IFM Investors Pty Ltd., people familiar with the matter said at the time.

Brookfield Asset Management Inc., which was said to be another bidder on the joint venture and eventually became one of Kinder Morgan Canada’s largest investors, could be a potential partner in Trans Mountain now. The Toronto-based alternative-asset manager already has a joint venture with Kinder Morgan, Natural Gas Pipeline Company of America, through its publicly traded Brookfield Infrastructure Partners. A representative declined to comment.

Among pension funds, the Ontario Municipal Employees Retirement System and the Alberta Investment Management Corp. could also be interested in the project. OMERS’ infrastructure arm is invested in several pipeline assets, including the Czech Republic’s NET4GAS sro, CLH Pipeline System in the U.K. and Spain, as well as the U.K.’s Scotia Gas Networks.

Midstream Veteran

OMERS also appointed Michael Ryder as the senior managing director of its infrastructure unit, OMERS Infrastructure. Ryder joined in January from U.S. private equity giant Blackstone Group LP, where he was responsible for leading the firm’s midstream energy and oilfield services investment strategy. A representative for the fund declined to comment.

AIMCo, as the Alberta fund is known, is supportive of measures to boost investor confidence and address market uncertainty, Denes Nemeth, a spokesman for the fund, said in an email, while declining to comment on whether AIMCo would be interested in investing in the project.

Canada Pension Plan Investment Board, the country’s largest pension fund, said in an emailed statement it was not “actively assessing an investment in the extension opportunity."

Largest Investor

Meanwhile, Caisse de Depot et Placement du Quebec, Canada’s second-largest pension fund, last month disclosed holdings of 10.2 million shares in Kinder Morgan Canada, making it the largest investor outside of its parent company. A spokesman declined to comment on whether the Caisse would consider an investment in the Trans Mountain pipeline Tuesday.

Caisse Chief Executive Officer Michael Sabia told reporters last week in Montreal that the Kinder Morgan investment was made prior to the pension fund announcing a new strategy in October to reduce its holdings in carbon-intensive industries in favor of renewable energy. He said last week that the Kinder Morgan Canada investment, along with all future investments, would be reviewed in light of the new policy.

After Kinder said it was halting work on the project until it had more certainty, the province of Alberta was named as a potential buyer for all or part of the project. Premier Rachel Notley said at the time that the province would consider all options for ensuring the project was built. “At this point, we don’t think that’s necessary,” she said Tuesday.

Other Projects

Canada’s other major pipeline operators are not seen as likely to enter the fray, either. Enbridge Inc. and TransCanada Corp., both based in Calgary, already operate major pipelines that carry oil-sands crude, and both are enmeshed in their own major projects. TransCanada’s proposed Keystone XL pipeline has battled delays for roughly a decade, and Enbridge’s Line 3 replacement and expansion still hinges on a critical regulatory ruling in Minnesota.

TransCanada spokesman Grady Semmens said in an e-mailed statement that the company isn’t involved in discussions about the Trans Mountain pipeline, and that it won’t comment further about speculation on the project. Suzanne Wilton, a spokeswoman for Enbridge, said the company is focused on its C$22 billion growth program and would not speculate on the project.

Bad Timing

The time is not right for either company to take on a project like Trans Mountain, said Laura Lau, who helps manage C$1.5 billion in assets, including shares of TransCanada and Enbridge, at Brompton Corp. in Toronto. Enbridge has been selling assets to help whittle down debt it took on in last year’s purchase of Spectra Energy Corp. TransCanada would be more able to buy it, but the company had its credit rating cut by Standard & Poor’s earlier this month, she said.

The purchase also would distract and draw resources away from their current projects, which Lau said she’s optimistic will go through.

“If they buy Trans Mountain, they have to not do something else,” Lau said in an interview. “There’s only so much money to go around.”

--With assistance from Naureen S. Malik and Greg Quinn.

To contact the reporters on this story: Scott Deveau in New York at sdeveau2@bloomberg.net;Kevin Orland in Calgary at korland@bloomberg.net;Josh Wingrove in Ottawa at jwingrove4@bloomberg.net

To contact the editors responsible for this story: David Scanlan at dscanlan@bloomberg.net, Carlos Caminada, Reg Gale

©2018 Bloomberg L.P.