French Banking Giant Is Looking Like ‘the JPMorgan of Europe’

French Banking Giant Is Looking Like ‘the JPMorgan of Europe’

(Bloomberg Markets) -- Jean-Laurent Bonnafé has heard all the reports, all the speculation. For months now, the market has been buzzing with the possibility that his bank, BNP Paribas SA, might take a run at acquiring a beleaguered competitor,Commerzbank AG. And why not? The Frankfurt-based bank has been struggling to find its footing even as France’s biggest lender, brimming with profits, has been pushing hard into Germany’s industrial heartland on the hunt for corporate clients.

So is it true?

Bonnafé, a 25-year BNP veteran of stolid technocratic bearing, frowns at the question. It’s a rainy spring morning in Paris, and the chief executive officer is sitting in a salon in the bank’s palatial headquarters at a table bearing baskets of freshly baked croissants and silver pots of coffee. He shakes his head.

“No, no, no. At this moment, you cannot take on large transactions,” Bonnafé says in French-accented English. The reason, he explains, is that BNP Paribas is investing €3 billion ($3.5 billion) to change how it uses technology, deals with customers, and develops new products. Assimilating the digital plumbing of Germany’s second-biggest listed bank would set that effort back two to three years. “If you do that, you cannot deliver on the digital transformation,” he says. “It’s as simple as that.”

But what if the price was right, regulators in both countries favored the deal, and other potential suitors were circling Commerzbank? Surely an IT project wouldn’t deter a blockbuster merger that would redraw the financial map of Europe. Bonnafé smiles, and with his analytical gaze he looks every part the engineer he trained to be.

“We are not children,” he says, sotto voce but firmly.

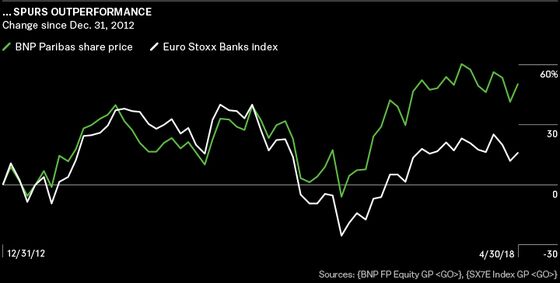

It’s true; the most influential commercial banker in the euro zone isn’t the type to be lured by shiny baubles. Ever since he took over as CEO in 2011, Bonnafé has shunned the glory hunting that’s long defined global banking. His watchword has been “discipline,” and while there have been aberrations—BNP Paribas pleaded guilty to processing transactions for clients in violation of U.S. sanctions on Sudan, Iran, and Cuba and paid $8.9 billion in penalties in 2014—this trait has enabled the lender to steadily take market share from its European competitors and increase its bottom line. Over the past five years through yesterday, BNP shares have outperformed those of most major European lenders, returning 8 percent annually, compared with 3 percent by the Euro Stoxx Banks index.

The story of the past decade in European banking has been one of calamity followed by fitful recovery. The German banks are still reorganizing, the biggest Swiss ones are returning to their roots in wealth management, the British are grappling with Brexit, and Italians are finally digging out of a mountain of bad loans. As the debris is cleared away, it’s BNP Paribas, a 196-year-old institution long overlooked as an appendage of the French state, that’s emerged as the closest thing the Continent has to a banking champion. With €2.1 trillion in assets, BNP is the euro zone’s biggest financial supermarket. It plies millions of customers on five continents with everything from auto loans, checking accounts, and equity derivatives to mergers-and-acquisitions advice.

“It’s the JPMorgan of Europe,” says Davide Serra, the CEO of Algebris Investments, a company in London that holds BNP shares and bonds. “Bonnafé’s approach has been ‘Keep it simple, keep it strong, keep it focused,’ and that’s a contrast with Deutsche Bank and Barclays, which seem to do endless strategic overhauls and new business plans.”

BNP is hitting its stride just as France itself is striving to shake off years of malaise and kick-start a more dynamic economy. French corporate leaders, including BNP Chairman Jean Lemierre, have been surprised at how swiftly President Emmanuel Macron pushed through pro-business reforms of the tax code and labor rules that were once considered virtually impossible. Macron is squaring off against powerful transportation unions in a series of work stoppages, and his detractors are wagering that his “En Marche!” agenda will ultimately fizzle out.

Yet Lemierre says the elevation of an outsider who never held elected office shows how fed up the French people are with the status quo. The 40-year-old president has already kindled optimism that France can change and hasn’t been shy about taking a turn on the world stage as an unabashed champion of a unified Europe. Asked if the “French moment” has finally arrived, Lemierre, the ever-diplomatic former president of the European Bank for Reconstruction and Development, pauses for a second. “It’s a Franco-German moment,” he says.

Maybe so, but the trajectories of the two biggest banks in the euro zone’s two biggest economies are veering off in opposite directions. For years, Deutsche Bank AG challenged Goldman Sachs Group, Morgan Stanley, and JPMorgan Chase for supremacy in the great game of global finance. But the credit crunch, coupled with Deutsche Bank’s swashbuckling culture, saddled it with legal scandals and heavy losses. Its long struggle to recover shows no sign of ending. In May, CEO Christian Sewing said the lender would pull back from the U.S. as part of a sweeping overhaul that could result in thousands of job cuts.

BNP took what turned out to be a more prudent path. It embraced staples: consumer finance, retail banking, corporate lending, custody services, and cash management. Not the sexiest stuff, but the kind of banking that customers need day in, day out. Unlike the relentless drive for action at Deutsche Bank, the BNP trading floor was steeped in caution, much to the chagrin of American and British traders who were eager to bag riches in the markets, according to a former senior executive.

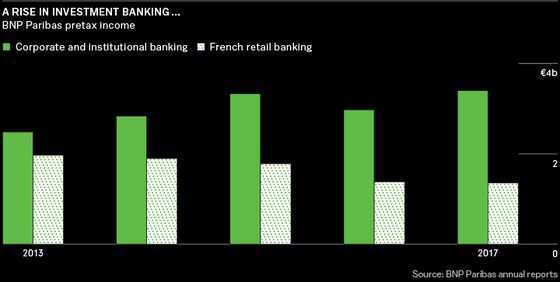

Now this steadfastness is paying off. BNP’s pretax income has climbed for three straight years, reaching €11.3 billion in 2017, which bested all competitors in the euro zone except Banco Santander SA, the Spanish retail banking giant. BNP’s first-quarter return on equity of 10.2 percent, a measure of how well it deploys its capital, is among the highest of Europe’s top 10 banks. And its markets business has been moving in the right direction. In 2017 it leapfrogged Barclays Plc and captured 5 percent of global trading in fixed-income, currencies, and commodities (FICC) business, compared with 4.7 percent in 2016. In equities, BNP outpaced the gains of virtually all major investment banks, including Goldman Sachs, with a 1.2 percent increase in market share.

Even so, the bank faces a raft of challenges that could upset this momentum. It suffered a bruising first quarter, with revenue in its FICC business sliding 31 percent from the same period in 2017, even as some U.S. rivals recorded solid gains. BNP chalked up the poor showing to a lack of demand for trading such securities in Europe, contributing to an 18 percent fall in pretax income for the group as a whole from the same period in 2017. What’s more, the retail banking unit in France has been a middling performer in recent years. Pretax income in 2017 came in at almost €1.4 billion, a 31 percent decrease since 2013, and its cost-to-income ratio has increased 7 percentage points, to 73.3 percent.

Some investors grumble that the bank could do a better job at cutting costs. “BNP is a high-quality, risk-managed institution that generates decent returns, but it is perceived as an arm of the French state,” says Barrington Pitt Miller, a portfolio manager at Janus Henderson Group Plc, an investment company in London that holds about 3 million of the bank’s shares. “There’s a sense that at times the balance sheet may not shrink when you may like it to because it has to be there for French interests around the world.”

France’s sluggish 0.3 percent growth rate in the first quarter is also fanning worries that the European Union’s economic recovery might be faltering. A slowdown could in turn prompt the European Central Bank to hold off on raising interest rates, as the Bank of England did on May 10, which would be bad news for lenders eager to charge borrowers more for loans. Algebris’s Serra would like to see Bonnafé acquire banks in Italy and increase loans to small and midsize businesses to bolster BNP’s Banca Nazionale del Lavoro SpA division there. BNL remains Italy’s sixth-largest bank by assets some 12 years after the French bank bought it.

Nonetheless, Bonnafé and his senior management team, who granted Bloomberg Markets a series of exclusive interviews, are running something rare in Europe: a sprawling financial emporium that’s primed for expansion. “As competitors pull out of markets, BNP can go in and win customers and take market share,” says Jason Long, a partner at Harris Associates LP, an investment company in Chicago and one of BNP’s top 10 stockholders. “When you look at Deutsche Bank, that’s exhibit A.”

On an April morning inside BNP’s headquarters in central Paris, Bonnafé has every reason to believe the center of gravity in European banking is shifting his way. The 18th century neo-Renaissance mansion exudes the Gallic ambitions of another era. But Bonnafé, who removes his gray suit jacket and drains a glass of orange juice as he settles in for an interview, refrains from describing his business in terms of conquest and triumph. “This is not about becoming a champion. This is not the Olympic Games,” he says. “This is banking. Banking is about history and numbers. It’s an industry in which you have to survive the cycle. You have to have the ability to go through cycles and deliver a full scope of services in a number of geographies. Anything else is just funny, it’s just being ‘brilliant.’ It’s not banking.”

A graduate of the Ecole Polytechnique and the Ecole des Mines, two of France’s elite training grounds, he started his career as a civil servant in the Ministry of Industry. Bonnafé joined what was then called Banque Nationale de Paris in 1993, the same year the French government privatized the lender. In time he became the bank’s go-to executive for integrating acquisitions. In 2000 he managed the union of BNP and the Paris-based investment bank Paribas following a three-way takeover battle with crosstown rival Société Générale SA. (Bonnafé, who turns 57 in July, is quick to correct those who refer to the bank as just BNP: “It’s BNP Paribas.”)

He was then assigned to head the assimilation of BNL in Rome in 2006. Three years later came Fortis. The Dutch-Belgian lender was crippled by taking part in the €72 billion purchase of Dutch giant ABN Amro Holding NV in 2007, the disastrous deal that also poleaxed the Royal Bank of Scotland Group Plc. After Fortis was bailed out, BNP acquired the bank’s businesses in Belgium and Luxembourg, and today the Belgian state remains BNP’s No. 1 stockholder with a 7.7 percent stake. Few investors were surprised when Bonnafé succeeded Baudouin Prot as CEO in 2011.

His first order of business was dealing with the new realities of a post-crash world. In August 2007, BNP froze three funds with €1.6 billion in assets that were exposed to the collapsing subprime mortgage market. The move, mirrored by other companies at the time, was a watershed moment in the epochal events that were to follow. BNP, which wasn’t as aggressive as rivals such as Citigroup, Deutsche Bank, or UBS, avoided the worst of the fallout.

But Bonnafé faced pressing questions as regulators directed lenders to muster more capital to cover lending risk and build up liquidity buffers to absorb shocks. In 2011 the bank started deleveraging its balance sheet. Three years later, Bonnafé unveiled a growth plan rife with assorted revenue and cost-cutting targets. Yet behind the graphs lay a fundamental question: How will the European economy be financed over the next quarter century?

Companies on the Continent have long relied on bank funding more than capital markets. A 2015 study by the Boston Consulting Group Inc. found that loans to corporations accounted for 55 percent of the euro area’s gross domestic product, compared with 15 percent in the U.S. American companies issued bonds at three times the rate of euro zone firms, and the €10 trillion in listed equity capital in Europe was about half that in the U.S.

Bonnafé bet that this imbalance would have to change and that BNP’s corporate bank would reap more in fees. In 2014 he tapped Yann Gérardin, a BNP lifer, to head the Corporate & Institutional Banking division and carry out this plan. Gérardin, who set up the bank’s equity-derivatives desk, hung a huge photograph on the wall of his office depicting the moss-covered interior of a derelict automaking plant in Michigan. It’s still there. “I tell visitors that if we don’t change, this will be the future of the bank,” he says. He’s only half-joking.

Gérardin pursued a bottom-up approach to win new corporate customers, especially capital-hungry manufacturers in Germany’s Mittelstand, the stratum of midsize enterprises that forms the nation’s economic backbone. The idea was to start by helping companies manage their daily cash transactions and then move them on to more lucrative offerings. “If we are clever enough, next year you’ll use us for foreign exchange, and then maybe an interest rate hedging product, and a bond issue after that,” Gérardin, 56, says. “So the onboarding of today is the market share gain of tomorrow, asset class by asset class.”

BNP’s German headquarters is located on the site of an old freight depot in the shadow of skyscrapers in Frankfurt’s financial district. It’s here, in a boxy glass structure, that Lutz Diederichs, a 30-year veteran of German commercial banking, is challenging German lenders on their own turf. The abrupt departures of Deutsche Bank CEO John Cryan and his deputy Marcus Schenck in April, both dealmakers with extensive relationships in corporate Germany, would appear to present Diederichs with an opening, though he’s careful not to overreach. “Do we necessarily need to be No. 1? No, but for the German Mittelstand you have to be among the top three banks,” says the banker, who joined in 2017 after a long tenure at HVB, the Bavarian bank owned by Italy’s UniCredit SpA.

Diederichs does have a lot to work with. He runs 13 separate businesses, including wealth management, real estate brokerage, and securities services. He also oversees eight “houses” in Berlin, Stuttgart, Hanover, and other industrial centers. They’re not small; the Munich one has more than 100 financial professionals.

By underpricing competitors, Diederichs says, he’s willing to compromise profitability to win market share. Last year revenue in Germany jumped 13 percent after increases averaging 8 percent a year from 2012 to 2016, says Diederichs. His goal is to generate €1 billion in sales from corporate clients by 2020. But even if he reaches his target, BNP would still be a second-tier player in Germany; Commerzbank recorded almost €1 billion in revenue from its corporate clients in the first quarter alone. As tempting as it might be to use an acquisition to scale up, Bonnafé is wise to be prudent, say analysts. “If Commerzbank or any other sizable target comes to market, the conditions would have to be very attractive for BNP to justify taking a risk,” says Jon Peace, a London-based analyst at Credit Suisse Group AG.

The bank’s full-court press may be hard to sustain over the long term in a market where many local players scratch for profits amid subzero interest rates and intense competition. The bank has made a big wager that proximity to potential German clients will pay off. With all its bricks and mortar and multiple businesses, it’s going to be tough to control expenses. Diederichs may also find it challenging to raise prices on services after slashing them to capture market share. Not to be outdone, Commerzbank is intensifying its efforts to win new corporate customers, and Deutsche Bank is hiring senior bankers from Morgan Stanley and Goldman Sachs in Frankfurt as it refocuses on its home market.

BNP did bag a watershed deal in March. Along with Perella Weinberg Partners LP in New York, the bank advised E.ON SE, a power supplier based in Essen, Germany, in its €22 billion acquisition of Innogy SE. It was a game changer for the German energy industry, and there were no German banks in the mix, something the nation’s CEOs will notice. “Five years ago they never would have thought about BNP Paribas in a deal like that,” Diederichs says.

Across the Atlantic, in a suite of offices high above Midtown Manhattan, Jean-Yves Fillion is facing a very different situation: a marketplace dominated by juggernauts such as Goldman Sachs, JPMorgan Chase, and Morgan Stanley. Fillion, CEO of the French bank’s U.S. holding company and head of its corporate and institutional bank in the States, oversees a sizable operation that dates back to the late 1800s. On one side is Bank of the West, a San Francisco-based retail banking operation with $69.7 billion in deposits and 2 million customers in 23 states. On the other is the corporate bank, which is run out of New York and recorded about $2.5 billion in revenue in 2017.

Being in the U.S. is critical to a bank with European multinational clients. Yet Fillion says BNP Paribas has resisted the urge to try to match the U.S. banks product by product. “We have the second-biggest balance sheet in the group outside of France, and we put it to work. But when you compete against the American banks, you’d better be selective,” he says. “If you are not, you might have to do what I have seen other banks do over the last two years: You shrink, you retreat, you lose your relevance. Believe me, I am not casting any stones here.”

Fillion’s operation is content to play to its strengths, and lately that’s meant selling derivatives, long a specialty of the French banks. The recent surge in market volatility has prompted corporate clients to ask for instruments that help them hedge risk. In the fourth quarter the bank had $211 billion in equity-based derivatives and similar contracts, marking a steep rise from 2015, according to records at the U.S. Office of the Comptroller of the Currency. In the equity-derivatives rankings, BNP is running right behind JPMorgan Chase, Goldman Sachs, and Société Générale, according to data from Coalition Development Ltd., a research firm in London. A 19 percent spike in BNP’s equity-derivative and prime-brokerage sales in the first quarter helped the global markets business partly offset the slide in FICC revenue.

BNP’s U.S. team also muscled its way into a market where it had not played a significant role before: collateralized loan and debt obligations. These fee-rich instruments, which are pools of debt sliced into tranches ranked by risk, played a titanic role in exacerbating the subprime mortgage crash of 2007-08. In 2017 the bank originated and distributed more than $9 billion worth of CLOs and CDOs, making it the No. 6 company in the space, Fillion says.

Harris Associates’ Long says he’s keeping a close eye on this part of the business. “What would raise a red flag is if the derivatives book started growing more than the rest of the bank,” he says. Fillion says that isn’t going to happen. “These products became toxic when they were made for pure speculation, vs. solving the true economic need of a client,” the banker says. “That’s why we have remained steady in the derivatives space.”

Ensconced in a plain white office with panoramic views of Parisian rooftops, Sophie Heller is playing a key role in Bonnafé’s €3 billion digital transformation project. She’s chief operating officer of the retail banking and services unit, so the changing needs of customers are very much on her mind. Wielding an iPad loaded with PowerPoint decks, Heller runs through a number of innovations roiling the lending business, including smartphones, machine learning, and cloud computing. She peppers her conversation with references to “optimization,” “net promoter scores,” and “rebalancing channels.”

But the bottom line is pretty simple. “The customer experience has become the new battlefield,” says Heller, the former head of retail banking for the French digital banking business of Dutch lender ING Groep NV. The bank plans to use artificial intelligence programs to anticipate what other services account holders may welcome on their “customer journeys” through its website or mobile app.

When it comes to fintech, though, BNP is lagging rivals such as Santander and Barclays, both of which overhauled their apps and branches years ago. Last July, Bonnafé approved the acquisition of Compte-Nickel, a French digital banking startup, for a reported €200 million, one of the biggest fintech deals in Europe of the year. (The bank declined to confirm the price.) Compte-Nickel lets consumers set up a bank account in about five minutes at thousands of newsstands and tobacco shops.

What sold Bonnafé on the deal wasn’t only that Compte-Nickel is reaching a customer base beyond his company’s range. It was also how the certainties of his business are becoming, well, less so. “There are ways to do day-to-day banking now without actually being a bank,” Bonnafé says. “You can imagine that in 20 years, the bank account may still exist, but its importance may shrink to nothing. You still have wealth, lending, payments.”

For Bonnafé, coming to grips with such existential questions is paramount. The man who thinks about banking in terms of surviving the next cycle draws comfort from the decision the bank made long ago to stay intact and to remain a financial supermarket. Now, as Macron asserts France’s unifying role in Europe, it’s hard not to see an auxiliary role for the country’s biggest bank. “If Europe believes in Europe, then it needs a continental bank with a global corporate and institutional banking business,” says Pitt Miller of Janus Henderson. “Deutsche Bank may have been that once, but the potential over time is that BNP becomes the bank of Europe.”

Bonnafé might balk at such talk, but filling that role is his objective, stated or not. He and his team will do it their way, heads down, laboring for business slowly but surely. If Aesop were writing the fable of European banking, BNP Paribas would definitely not be the hare. Bonnafé doesn’t care. “Image and perception are the beginning of the problem in banking,” he says. “You have to deliver what your customers want. Anything else is not that important.”With that, the CEO rises, puts on his jacket, and walks into the courtyard at the center of BNP’s headquarters. He joins Chairman Lemierre and other directors from the board, who’re chatting in front of a large white backdrop flanked by studio lights as a photographer prepares to take their portrait for the next annual report. A luncheon will follow. The board members have much to discuss.

Robinson covers finance in London. Benedetti Valentini covers finance in Paris. With Steven Arons, Donal Griffin, and Yalman Onaran

To contact the editor responsible for this story: Stryker McGuire at smcguire12@bloomberg.net, Frank Connelly

©2018 Bloomberg L.P.