(Bloomberg Opinion) -- Elon Musk’s recent Twitter-lashing of the media has prompted comparisons to President Donald Trump’s “fake news” obsession. For me, though, its sheer variety — encompassing Soviet propaganda, a new Model Y launch date, the Theranos scandal, the lameness of car emoji, and much more — instead brought Steve Bannon to mind, particularly his media strategy: “flood the zone with shit.”

Intentional or not, having people debate the utility of journalists or the stability of Tesla Inc.’s chairman and CEO, rather than just analyzing the company, seems like a useful-ish outcome. Recall that Musk similarly shot the messengers on the latest earnings call, dismissing valid questions as “dry.”

Psychoanalyzing Musk via social media is futile, of course. But the episode does resurface one pertinent question: How is Tesla’s board of directors doing?

They didn’t respond to a request for comment on this. Presumably, that isn’t because they haven’t thought about it. In the past three months, the chairman and CEO has lashed out at Wall Street and the media — two frequently supportive institutions — while struggling to fix a serious malfunction on Model 3 production; the stock has fallen about a fifth; and Tesla’s balance sheet looks, well, ripe for at least some discussion. How could you be a director and not think about it?

Thankfully, we have evidence at least one of them is paying attention:

Kimbal Musk, Elon’s brother, is the subject of calls by CtW Investment Group, an activist firm, to be voted off the board. Tesla has long been criticized for its paucity of truly independent directors. This was highlighted particularly in 2016’s acquisition of SolarCity Corp., a struggling vehicle chaired and partly owned by Elon Musk, indebted to his rocket company, Space Exploration Technologies Corp., and run by his cousin. It has boosted Tesla's leverage significantly and sparked an investor lawsuit that a judge recently ruled could proceed, saying conflicts “diminished the board’s resistance to Musk’s influence”.

In the wake of that, the board got some new blood last year in the form of Linda Johnson Rice and James Murdoch, who run Johnson Publishing Co. and Twenty-First Century Fox Inc., respectively (seems the media isn’t all bad). However, Tesla recommends Kimbal Musk remain a director and resists calls to split the roles of chairman and CEO. And, as last week’s extended riff from Elon Musk — and his brother’s reaction — demonstrate, there’s scant evidence of the board acting as a real check or balance.

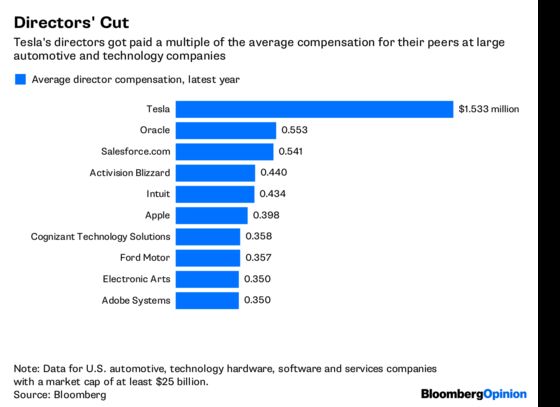

It isn’t as if the directors aren’t paid to do so; far from it. They were awarded an average of $1.53 million last year (Musk, as CEO, doesn’t get paid extra for being chairman). I ran a screen on the Bloomberg Terminal for average director compensation at U.S. automotive and technology hardware, software and services companies with a market cap of $25 billion or more, returning Tesla and 21 others. Here’s average director compensation for the top 10 payers:

To be clear, Tesla’s directors get most of their compensation as stock options rather than restricted stock or stock units, which predominate at the other companies. So those headline numbers depend on valuation models and are not directly comparable.

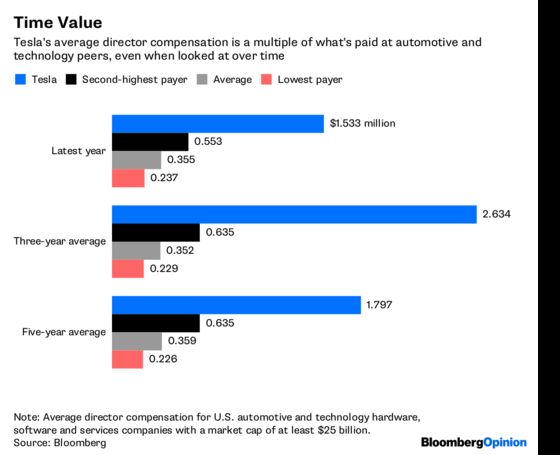

Rather, this is to illustrate that Tesla’s board pay, while aligned with growing the stock price, isn’t stingy. As Dan Marcec, director of content at compensation-analytics firm Equilar, put it to me: “Rarely do we see any director compensation valued at over a million dollars.” ISS also noted this issue in their recent report calling for governance reforms. And Tesla’s high average board compensation holds true over time, not just last year:

Now, Tesla’s directors only get paid if the stock performs well; and, on a five-year view, it has certainly done that, surging 819 percent between the end of 2012 and 2017. And the stock is, of course, the crux of the issue.

Tesla’s success or failure is widely perceived to be synonymous with that of Musk himself. The paradox here is that belief in Musk has girded Tesla’s valuation in the face of chronic losses and, especially lately, missed targets — which actually makes Musk’s presence seem all the more essential, since that high valuation enables the company to raise the capital it needs. It’s like a $47 billion treadmill. Thus, any attempt to rein in Musk, even textbook stuff like appointing an independent chairman or curtailing his Twitter privileges, appears to risk Tesla’s valuation and, thereby, its future.

This is not a reassuring situation. As Musk’s own recent admission of his costly mistake around factory automation demonstrates, even geniuses can use occasional pushback. Tesla’s stock has benefited from Musk’s aura, but that also leaves it vulnerable to that aura dimming. And while many applaud Musk’s combativeness, it is also unnerving; you just don’t often see CEOs of major companies acting this way, especially when they are supposedly laser-focused on fixing urgent problems.

All of which leaves Tesla’s board, as it currently stands, something of a curio. For those who think Musk should just keep being Musk, it appears largely irrelevant. And for those seeking signs of more robust supervision, you could say much the same thing.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

©2018 Bloomberg L.P.