Biopharma Deploying Trump Windfall to Buy Back Billions in Stock

Biopharma Deploying Trump Windfall to Buy Back Billions in Stock

(Bloomberg) -- Drugmakers, whose industry pricing faced renewed scorn this month from President Donald Trump, have been taking advantage of the U.S. tax overhaul he signed last year to buy back shares of their own underperforming stocks.

Large-cap biopharmaceutical companies took advantage of repatriation of overseas profits and lower corporate tax rates to push share repurchases to the highest level in at least 10 years. Companies led by Amgen Inc. and Pfizer Inc. bought back a combined $16.7 billion in the most recent quarter, according to data compiled by Bloomberg. And they’re not done. Celgene Corp., whose market value has been cut in half over the course of about seven months, on Thursday boosted its repurchase capacity by $3 billion and planned a $2 billion accelerated buyback.

These biopharma leaders have so far confounded investor expectations for a big pickup in mergers and acquisitions, opting instead to help their earnings per share while taking advantage of their struggling stocks. That might make sense for a group that’s under increasing pressure to deliver strong quarterly results amid rhetoric from the Trump administration about their drug pricing.

“There is pressure from investors to do something with their cash, and if there’s not a great target to add assets to your pipeline, then a buyback will look more attractive,” Credit Suisse analyst Vamil Divan said in a telephone interview. “A lot of these companies have limited growth outlooks in the near-term, so buybacks are a sure way to give yourself a bump if you don’t want to take on risk just yet.”

The larger group has struggled to find its footing in recent months. Biotechnology companies in the S&P 500 have fallen close to 5 percent to start this year while pharmaceutical stocks sank closer to 6 percent despite the broader S&P 500 edging up 2 percent.

Biotech investors came into the year hoping for a wave of deals, spurred by corporate tax reform that left companies with fatter wallets. More capital hasn’t translated into more deals, though, forcing investors to position themselves in potential targets instead.

Leerink analyst Geoffrey Porges blames “lazy balance sheets” for the lack of deals, since companies could create some $460 billion in deal capacity by issuing debt to augment their dry powder.

“In the large-cap space, cash has never been a problem,” Peter Collum, a partner at MTS Health Partners who advises on life sciences deals, said in an interview at his New York office. “They have and continue to have access to cash, so an increase in availability is not a binary switch to prompt buying, especially when valuations for commercial-ready medicines are this high.”

That isn’t to say the well ran dry for international mergers and acquisitions to start the year. Osaka, Japan-based Takeda Pharmaceutical Co. agreed to buy much-larger rival Shire Plc in a $62 billion deal and Novartis AG of Basel, Switzerland, acquired gene therapy company AveXis Inc. for about $8.7 billion. However, the group of top North American biopharma stocks saw deals fall back in-line with recent trends so far this year after hitting a low to end 2017.

Enter buybacks and tender offers, such as the Dutch auction for up to $7.5 billion in stock that AbbVie Inc. began at the beginning of May. The move has lifted shares, putting the company on pace for its best monthly performance since January. Divan noted that the drugmaker made it “very clear that they felt the stock was undervalued after Rova T data.”

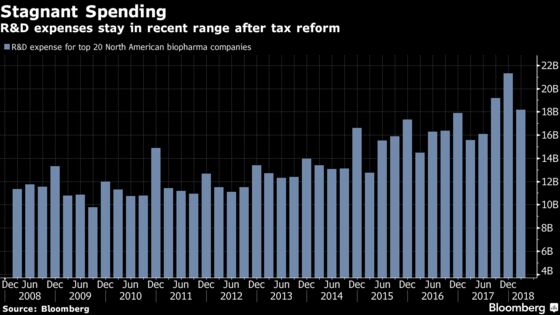

Congressional Republicans have argued that cutting taxes would spur an increase in investments by American companies and fuel innovation. Data compiled by Bloomberg on research by the top 20 drugmakers show that while R&D spending grew year-over-year in the first quarter, it remains below quarterly levels seen in the second half of 2017 and comparable to the the fourth quarter of 2016.

To be sure, it can be quicker to use buybacks for rewarding shareholders, while waiting for in-house drug development to pay off or scouting promising therapies discovered elsewhere.

“It’s a good thing to do because it can return money to shareholders in a very easy and tax friendly way,” William Blair analyst Matt Phipps said by phone. “But it has to be part of a balanced capital strategy where you can shore up your pipeline.”

--With assistance from Javon Thompson, Seth Pitkow, Jeffrey Hernandez, Karishma Motwani, Taka Endo and Anthony Fasanella.

To contact the reporter on this story: Bailey Lipschultz in New York at blipschultz@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Jeremy R. Cooke, Scott Schnipper

©2018 Bloomberg L.P.