Tech or Retail? Ocado's U.S. Deal Gives It Amazon-Like Valuation

Tech or Retail? Ocado's U.S. Deal Gives It Amazon-Like Valuation

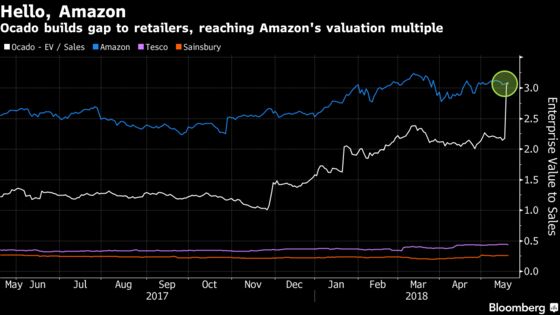

(Bloomberg) -- As an online grocer, Ocado Group Plc has always commanded a higher valuation than traditional retailers. But last week’s U.S. deal puts its valuation multiples squarely in-line with Amazon.com Inc., and leagues away from the likes of Tesco Plc and J Sainsbury Plc.

The company’s landmark technology-licensing deal with Kroger Co. sent the shares up 44 percent on Thursday, squeezing short sellers and putting the ratio of Ocado’s enterprise value to sales above three, similar to internet giant Amazon. Tesco and Sainsbury both have ratios of less than 0.5.

Enterprise value divided by sales -- a metric sometimes used to value high-growth software companies -- provides a more useful gauge at the moment than Ocado’s stratospheric price-to-earnings ratio. Measuring the market capitalization plus debt minus cash against estimated revenue sheds some light on what kind of growth investors now expect from the company.

It’s a change in fortunes for Ocado -- an IPO some investors said took an “act of faith” to invest in. After losing 70 percent of its value during its first 18 months as a publicly traded entity through 2011, the stock’s market capitalization has more than tripled in the past six months, climbing above 5 billion pounds ($6.8 billion).

Ocado’s partnership with the second-biggest grocer in the U.S. may boost earnings before interest, taxes, depreciation and amortization by about 100 million pounds by 2020, bringing it almost 80 percent higher versus previous estimates, according to Marcus Diebel, an analyst at JPMorgan Cazenove.

Ocado’s licensing deals have also taken its enterprise value to Ebitda far beyond European online platform providers Just Eat Plc and Scout24 AG, which serve a different clientele, but have traded with similar multiples in the past. The current level of above 50 times Ebitda comes with the caveat that some analysts may not have included the most recent deal in their 12-month estimates, but illustrates the impact these pacts have had.

To contact the reporter on this story: Kasper Viita in London at kviita1@bloomberg.net

To contact the editors responsible for this story: Celeste Perri at cperri@bloomberg.net, Beth Mellor

©2018 Bloomberg L.P.