(Bloomberg Opinion) -- Conglomerates fell out of fashion because so many of them destroyed shareholder value: Companies boosted their top lines by deploying great wads of capital, but failed to earn a sufficient return. AP Moller-Maersk A/S is in danger of delivering another salient lesson for investors: Breaking up a conglomerate doesn’t necessarily create value either.

To recap, Maersk decided in 2016 to separate its energy and shipping activities so it could invest more in the latter. By now investors probably hoped to see some tangible benefits from all that upheaval, yet they’re pretty hard to spot.

Though comparable sales jumped 10 percent in the first quarter, that increase was to no obvious benefit. Maersk posted a $220 million quarterly loss from continuing operations as fuel costs rose faster than freight rates.

The businesses that Maersk is keeping account for tens of billions of dollars of invested capital yet earned a negative return of 0.6 percent during the three-month period. That’s worse than the same period a year earlier, and nautical miles off its target of about 8.5 percent.

Little wonder the shares tanked as much as 12 percent.

Maersk once viewed owning both oil and shipping assets as way to stabilize earnings: cash flows from rising oil prices offset the burden of increased shipping fuel costs. That was exposed as wishful thinking in 2015 when both container rates and oil prices collapsed. But having completed the sale of its North Sea oil business earlier this year, Maersk is now under more pressure to show it can pass on rising fuel and other variable costs to shipping customers.

At the moment, it’s struggling to do that because there is still a surplus of shipping capacity. Plus, every time U.S. president Donald Trump delivers another bombshell on trade, the stock gets buffeted, because the company controls about a fifth of container shipping flows. (For now, though, trade flows haven’t been affected too much by the president’s saber-rattling.)

In fairness, the full benefits from the promised $600 million of synergies from closer cooperation between the various shipping activities aren’t expected until the end of next year. Maersk’s investments to digitize a still-paper dominated industry also won’t pay off overnight.

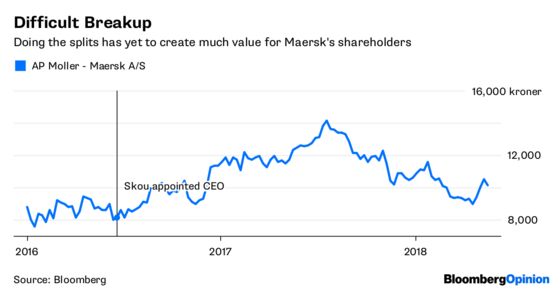

Chief Executive Officer Soren Skou could argue that the shares are about 12 percent higher now than when he was appointed almost two years ago and indicated the Danish company was considering a breakup.

He should resist. Oil prices have surged by 60 percent since then, while container rates have also rebounded, albeit by not nearly as much. These factors would probably have boosted Maersk’s value without Skou having to lift a finger.

Sensibly, Skou now plans to cut cost further and reduce freight capacity on routes that aren’t delivering sufficient returns. But that statement somewhat undermines his belief in the benefits of expanding in container shipping.

The invention of the 40-foot container delivered huge value for the global economy by cutting the costs of trade. Its ability to create value for the owners of those container ships looks as questionable as ever.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

©2018 Bloomberg L.P.