What Does $3 Billion Even Buy Tesla These Days?

(Bloomberg Opinion) -- Tesla Inc. says it doesn’t need to raise more money. But a new report from a usually supportive quarter suggests it not only should, but really, really should.

Adam Jonas, a Morgan Stanley analyst who typically rates Tesla stock with gusto, just slashed his target price 23 percent to $291 —curiously, within a buck of where it closed the night before. The stock duly dropped about 3 percent on Tuesday.

There are a clutch of interesting things to note about Jonas’s report. For example, despite the hammered target price and the earnings estimate for 2019 going *poof* from a positive $1.31 per share to a negative $4.69 — before counting stock-based compensation — Jonas’s Tesla rating is still effectively a “hold.” There is also the useful fact that about a third of that new $291 price target relates to “Tesla Mobility,” a robo-taxi business that doesn’t yet — how to put this? — exist.

But about that new fundraising.

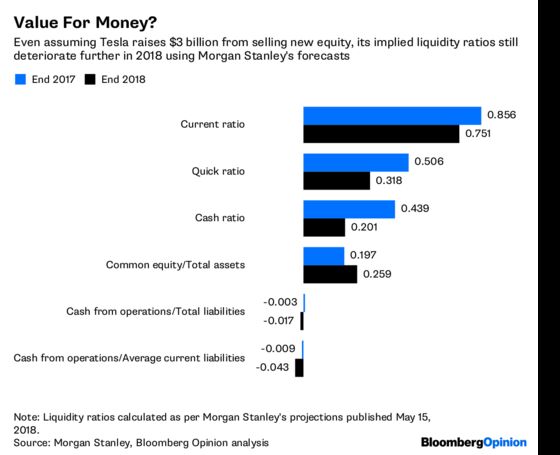

Jonas now expects Tesla to tap investors for $3 billion in the third quarter, up from an earlier estimate of $2.5 billion. The kicker, though, is that $3 billion doesn’t really do much for Tesla’s strained balance sheet these days.

The only one that improves there is common equity versus total assets — but then, selling $3 billion of new common equity will tend to do that for you. Meanwhile, the top three ratios, already in undesirable sub-1.0 territory, slip further. And clearly, the bottom two in the chart have those unwelcome minus signs in front of them, reflecting actual and expected negative cash from operations.

This shouldn’t be surprising. Recall that Tesla’s working capital is deeply negative — to the tune of $2.27 billion at the end of March — and its leverage, both on and off the balance sheet, has continued to climb. Any new equity raise would have to be substantial to offset those obligations and get Tesla’s ratios looking healthier.

But a bull probably wouldn’t look at it that way. Rather, they would see the next $3 billion as a short-term bridge to a place where Tesla has fixed its Model 3 problems and cash from operations starts doing the heavy lifting. This is the crux of the bull thesis: Sustained profitability, however deferred to date, remains just around the corner, and Tesla’s giant market cap provides the reserve tank (battery?) to get there.

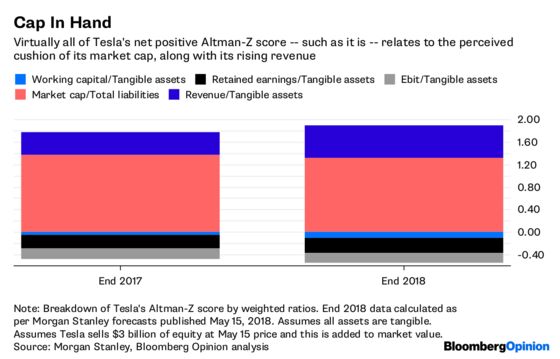

You can see evidence of this in Tesla’s Altman Z-Score, a weighted average of five ratios where a score of less than 1.8 can indicate a high risk of bankruptcy . Tesla scored 1.3 at the end of 2017 and, using Morgan Stanley’s numbers, would theoretically end 2018 at somewhere between 1.27 to 1.35, depending on how one treats the equity sale’s impact on the market cap.

Again, the $3 billion infusion doesn’t really move that needle. More importantly, though, in the absence of positive profits and with working capital so negative, virtually all of Tesla’s Z-score is a function of that market cap:

And the thing is, a big market cap is powerful; Tesla is living proof. But to simply focus on that while ignoring the slow drip of faltering liquidity ratios is to run a colossal risk and put a lot of trust in your fellow shareholders keeping their nerve.

All of which makes Morgan Stanley’s target-price cut unhelpful, especially as the bank has led previous capital rounds and analysts have turned a bit more skeptical in general. A year ago, Wall Street’s “buys” outnumbered “sell” ratings almost two-to-one, according to data compiled by Bloomberg. Today, the stock is slightly lower and buys and sells are almost neck and neck.

Until there is hard evidence of sustained progress on fixing the Model 3’s problems, Tesla relies on sheer belief. And as these latest estimates from a longstanding bull suggest, shoring up its balance sheet may require a bigger slug of belief than even the believers anticipate.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

©2018 Bloomberg L.P.