(Bloomberg View) -- The softening of U.S. sanctions against Russian aluminum producer Rusal sends at least two important signals to investors and to official Moscow. One is that the Trump administration has little understanding of the impact of its moves before it makes them. The other is that it doesn't want to impose sanctions that will do a lot of collateral damage outside Russia.

These peculiarities of the U.S. sanctions policy are both a blessing and a curse for President Vladimir Putin's Russia. The trial and error nature of the policy means any individual (and his or her companies) can be hit at any time, especially if they have the misfortune to appear on Forbes Russia's list, used by the U.S. Treasury Department as a master list of sanctionable "oligarchs." But the U.S. unwillingness to inflict damage on its "partners and allies," whose interests Treasury Secretary Steven Mnuchin mentioned as the reason for his retreat on Rusal, sends an unmistakable message to Russian companies and the Russian state: spreading operations internationally is an effective way to discourage sanctions. That's good to know for both strategic and tactical purposes.

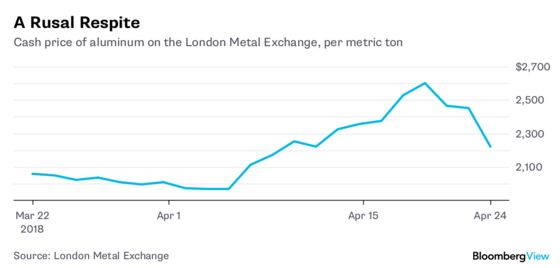

The sanctions against Rusal's biggest shareholder Oleg Deripaska and his assets were the first truly effective U.S. restrictions against Russia. By effectively banning Rusal from doing business in U.S. dollars and thus from exporting aluminum to the U.S., the Trump administration forced the world's second biggest producer of the metal to find new markets for metal that provided 14.4 percent of its revenue last year. The blow's seeming randomness -- it wasn't clear why Deripaska was picked first for such harsh punishment -- spooked investors, and Russian shares plummeted across the board.

I remain convinced that Deripaska was chosen because his company deals in aluminum -- the target of Trump's import tariffs, which are meant to revive domestic production. The opportunity to kill two birds with one stone -- punish Russia and get a major foreign player off the U.S. aluminum market -- must have looked too good to pass up. But no one in the Treasury Department appeared to have considered the consequences for the global aluminum market, where Rusal was included in international value chains. Aluminum prices jumped (which can only be bad for U.S. buyers), Australian-British Rio Tinto was forced to search frantically for new buyers for its alumina (a raw material for aluminum production), and a Rusal plant in Ireland was threatened with closure, creating the potential for job losses and an alumina shortage throughout Europe. These problems, reported to Treasury, appeared to soften Mnuchin's heart. "The U.S. government is not targeting the hardworking people who depend on Rusal and its subsidiaries,” his department quoted him as saying. The U.S. government's problem, Mnuchin said, was limited to Deripaska himself.

The new edition of the Rusal sanctions gives the company an extra six months, until October 23, to wind down its U.S. operations, but Mnuchin has clearly indicated that if Deripaska divests Rusal shares, the company could be taken off the sanctions list. Business partners will still be leery of dealing with Rusal, and they'll still work on contingency plans, but at least there'll be less urgency about it. That's been reflected in an aluminum price drop almost as sharp as the spike after the original sanctions announcement.

This is good news for Norilsk Nickel, part-owned by Deripaska and another Russian who made his fortune during privatizations in the 1990s, Vladimir Potanin. As the world's biggest supplier of nickel and palladium and a global top-10 copper producer, it should be safe: Sanctioning it would cause even more serious disruptions than in the Rusal case. It's also unlikely that the U.S. will hit Russian oil and gas companies, which play a major role in the global energy market, or Russian steel producers. The Russian government, too, can breathe a sigh of relief. Its sovereign debt, rated investment grade by Standard & Poor's since last February and widely held by institutional investors, is safe from sanctions, too.

There's a catch for both Russian billionaires and the government, though. The U.S. is essentially claiming the power to decide who should and shouldn't own Russian companies. Now, both Deripaska and the government will be interested in testing solutions to that problem. Will the U.S. relent if Deripaska hocks part of his stake to a state-owned Russian bank? Will a nominal sale to a proxy cut it? Or should Deripaska simply use the extra time to reorient the company completely away from the U.S. market and banking system, choosing defiantly to work only in Asia? My guess is that the company and the Russian government will look for a scheme that'll satisfy the U.S. without dispossessing Deripaska. If they find one, others will use it as a precautionary measure.

In any case, the U.S. foray into sanctions that really bite clearly hasn't been a success. It showed that hitting companies integrated into global markets can have too many unintended victims.

There is an obvious alternative the U.S. hasn't been serious about implementing. Mikhail Khodorkovsky, the former owner of Russia's top oil company and one of the Putin regime's most consistent opponents, laid it out in a column The Wall Street Journal published on April 22. "The West’s real enemy – and the enemy of the Russian people too – is a group of about 100 key beneficiaries of the Putin regime, and several thousand of their accomplices, many of whom hold posts in the Federal Security Service and the presidential administration," Khodorkovsky wrote, suggesting that the West must sanction these people, most of whom "began their careers in the criminal underworld of St. Petersburg."

These are emphatically not the oligarchs who got rich under Putin's predecessor, Boris Yeltsin. They are the real Putin cronies from his time in the KGB and the St. Petersburg mayor's office -- the people with the most shadowy influence on the Russian justice and law enforcement systems, the ones capable of taking away others' businesses and rigging major government tenders, the "new nobility" of the Putin era.

The U.S. has sanctioned some close Putin friends from the early days of his career, such as oil company Rosneft's Chief Executive Officer Igor Sechin, billionaire Gennady Timchenko and three members of the super-rich Rotenberg family. Whether or not they are members of the group Khodorkovsky describes, his proposal isn't about hitting a few fabulously wealthy individuals whose closeness to Putin is universally known. It's about patient investigative work to find out the identities of thousands of shadowy people getting rich off the Putin regime, finding their Western assets, freezing them before they can react and informing the public about these people's ties to Putin and his inner circle. That would send ripples throughout Russia, but not through important global markets.

Lazy formulas like the one used by the Treasury Department in the Deripaska -- "has been accused of threatening the lives of business rivals, illegally wiretapping a government official, and taking part in extortion and racketeering" -- only betray a lack of expertise. Anyone can find references to these accusations on the internet. Is that really the best the U.S. government can do? Following Khodorkovsky's advice, by contrast, could send serious chills up many backs in and around the Kremlin.

Most of the $1 trillion that has fled Russia to the West since the Soviet Union’s collapse isn't owned by the old-school "oligarchs." It was the corrupt officials and the little-known regime clients who moved it overseas. The West is still doing little to track that wealth and its owners; it's looking under the lamp, not in the shadows where the true criminals and their fortunes are. What happened to Rusal exposes this approach as deeply flawed.

Leonid Bershidsky is a Bloomberg View columnist. He was the founding editor of the Russian business daily Vedomosti and founded the opinion website Slon.ru.

To contact the editor responsible for this story: Mike Nizza at mnizza3@bloomberg.net.

For more columns from Bloomberg View, visit http://www.bloomberg.com/view.

©2018 Bloomberg L.P.