(Bloomberg View) -- The U.S. gross domestic product is poised to be disrupted, in the best way possible. Interruptions of the supply chain as a result of the recent series of natural disasters will lead to a huge buildup of inventories rebuild that will juice the math behind GDP growth in the months to come. Signs that the economy was beginning to slow will fade as quickly as they showed up.

While it’s intuitive that the natural disasters triggered a mass of delays in delivering supplies, the economy was already deeply undersupplied before Hurricane Harvey made landfall in late August. In the first half of the year, final demand increased by $237 billion but inventories rose only $7 billion. The hurricanes and California wildfires will only exacerbate the deficits that had been building.

The two most recent Institute for Supply Management reports were particularly eye-opening. Combining the manufacturing and services sectors, these reports show that a record 27 industries, accounting for about 70 percent of U.S. output, reported slower supplier delivery times in September. This dynamic barely budged in October, with 26 industries reporting they continued to experience slower delivery times.

Corroborating the ISM, the Chicago Purchasing Managers Index, which has surveyed the entire U.S. economy since the end of WWII, found that backlogs in October hit a 43-year high. Whether it is materials or labor or a combination of the two, the back orders illustrate that there are inadequate resources to fill orders. Undersupplies of this magnitude should lead to a grab for workers and materials that could quickly manifest in higher worker pay and a continued rise in input costs.

Not surprisingly, the economic regions of the country most directly impacted by natural disasters are feeling the pinch the most. One Dallas Fed district firm in the printing industry reported that mail volume from hundreds of customers was still down.

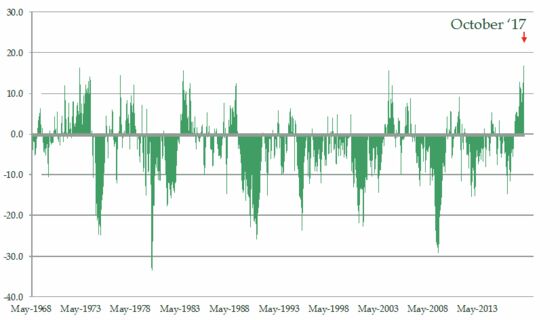

Whether the storms exacerbated the environment is difficult to pinpoint but the severe lag times are anything but contained to areas where the hurricanes made landfall. The Philadelphia Fed’s survey is a go-to for many economists due to its long track record back to the late 1960s. Echoing the national data, the Philly Fed also found record long delivery times in October.

Sitting Back and Waiting in Philly

Given its oversized role in trade, the California PMI provides a critical view of the global supply chain. The latest batch of data from the nation’s largest economy, California, tell us that the phenomenon extends beyond U.S. borders, and did well before wildfires ravaged much of the state.

There is a term economists apply to what’s in the making nationwide: “supply shock.” Shocks of any kind tend to show up quickly in inflation data, which should give investors pause. Policy makers at the Federal Reserve can debate the nuances of the ups and downs of monthly wage growth. But their attention will be instantly riveted by evidence in their industrial production and capacity utilization data that inflation risk has spiked due to the tremendous demand pulled forward at the very beginning of the supply chain.

None of this is to say inflation of the most nefarious sort, that of wages, is immune to a quick build in inflationary pressures. It still takes lots of workers to rebuild depleted inventories. The cost to carry temporary workers in the industrial sector was already running above that for temps overall. There’s only one way for wages to go in the near-term, which will no doubt squeeze margins further.

Temp Workers in Industrial Sector Will Continue to Command Wage Pricing Power

What’s a manufacturer to do? One California manufacturer lamented that the extra costs would have to be “absorbed," as in accept lower profits against a backdrop of their customers’ still-limited pricing power. Will this very real threat to the economy stop the Fed from aggressively pursuing inflationary pressures? That’s doubtful, given the cover an inflation spike would offer in fulfilling the central bank's commitment to continue hiking rates beyond its meeting in December.

Investors are unprepared for this inevitability. The difference between two-year and 10-year Treasury yields is 70 basis points, or 0.7 percentage point. That not only marks the lowest in a decade and the current cycle, but shows that markets are prepared for two quarter-point rate hikes at most. Supply shock or no, further rate hikes all but ensure the Fed will overtighten the economy in exactly the opposite direction of what the data is communicating.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Danielle DiMartino Booth, a former adviser to the president of the Dallas Fed, is the author of "Fed Up: An Insider's Take on Why the Federal Reserve Is Bad for America," and founder of Money Strong LLC.

To contact the editor responsible for this story: Max Berley at mberley@bloomberg.net.

For more columns from Bloomberg View, visit http://www.bloomberg.com/view.

©2017 Bloomberg L.P.