‘Textbook’ Bounce Doesn’t Stop for Speeches: Taking Stock

‘Textbook’ Bounce Doesn’t Stop for Speeches: Taking Stock

(Bloomberg) -- S&P futures dropped at 2 a.m. ET, but it had nothing to do with the State of the Union address, which mentioned little that was not previously telegraphed (vague mentions of infrastructure with little detail -- stocks to watch include materials and equipment firms EXP, USCR, MLM VMC, SUM, URI, HEES, HRI and even railroads like NSC, UNP). Attempts to lower drug pricing also was a focus, though details and nods to bipartisanship were scant, and as Raymond James points out, Senate Majority leader McConnell did not clap in support of the idea.

Instead, the little weakness seen this morning, barely down 2 handles of this writing, is coming off disappointing German data, which adds fuel to the idea that the Euro area is indeed slowing as the heart of that economy’s factory orders missed expectations.

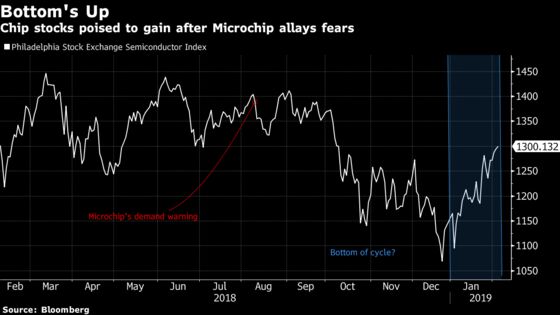

But the U.S. seems to be humming as a key weak spot late last year (semiconductors), looks to be turning a corner. Microchip Technology CEO in earnings post-market predicted the current quarter marked a cycle bottom, assuming U.S.-China relations remained steady. His comments, in conjunction with results from Apple supplier Skyworks (which beat on EPS, revenue and announced a $2 billion buyback program), should help lift one of the worst-hit sectors in trade today -- ON Semiconductor Corp., Texas Instruments Inc. and Marvell Technology Group all rose post-market.

Risky Business

Tuesday marked another day of risk-on (with the S&P 500 notching its 5th straight day of gains), and you can thank the Fed (still? from last week!) or whomever you like for giving the green light to buy growth equities. This catalyst-light week has lent itself to a melt-up of sorts with market watchers dumbfounded as to why we keep rising (is it FOMO?). I’ll give them the mystery of Alphabet’s reversal to go positive despite alarms on falling margins (which isn’t really a mystery as FAANG names tend to rise as one), but for all intents and purposes, we continue to get earnings results that let investors wipe their brow in relief.

The health of the consumer Tuesday? Check. Ralph Lauren had its best day since May while Estee Lauder rose the most in 7 years, while Sally Beauty also had good results. Capri (formerly Michael Kors just reported and raised its outlook and it’s up 2% in early trading). Disney just added to media-related bullishness in results post market (major media in the S&P have all beat on EPS expectations thus far), as did Snap (their user base was flat -- a good thing).

Its not all doom and gloom out there (when was the last time geopolitical trade issues with our biggest partner flared up?) The State of the Union speech also stayed away from any further detail on trade issues. We’ve even seen a few calls recently warning investors against some of the more defensive stances (low volatility, and bond proxies like utilities or REITs), with Barclays writing that the trade is was crowded and pricey.

Goldman Sachs strategists point out that investors have not yet fully rotated out of other safe haven assets (like gold, bonds) and into risk, similarly posing risks as those same assets would provide less "buffer" in the case of a true risk-off move. And low volatility names are expensive, Deutsche Bank writes, despite having "suffered the most" with the latest risk on environment and rotation towards growth.

With the most cautious among us "suffering" with below market gains as tech and discretionary takes off, its "too early to aggressively" move back in to low volatility Wells Fargo writes, even after the "textbook" January for risk assets.

Small Packing a Big Punch

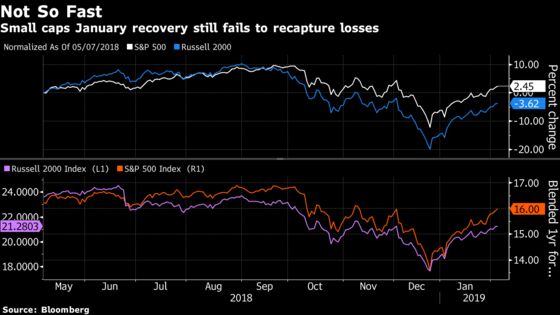

Part of that textbook performance was in the small caps. With more than 50% of the S&P 500 earnings in the books, its worth considering an attention pivot to some smaller names (just 25% of the Russell 2000 have reported thus far), especially given the extraordinary move in the index seen in recent weeks.

The Russell 2000 has outperformed this year (+12.7% to the S&P’s 9.2% gains), which shouldn’t come as too much of a surprise given how deep the losses ran into the end of 2018 and the resulting multiple compression. But you can also see in the above chart, that even with the rebound, RTY valuations on a blended 1-year forward P/E basis have yet to eclipse some of its latter half 2018 levels, while the S&P is nearing more normal territory.

Ultimately valuations will be the key to watch before this rally starts to stall. Morgan Stanley’s Wilson, who just last week recommended selling the January rally, wrote Monday that investors should seek out individual stocks as its now "time to be patient and wait for a better entry point."

Sectors in Focus Today

- Video game makers after Electronic Arts results sent shares down 17% and Take-Two Interactive raised their forecast for revenue but still missed estimates. Follows disappointing results from Glu Mobile earlier in the week

- Media after DIS results generally pleased; watch CBS, NFLX, DISCA

- Packaged meat players after reports that TSN was seeking to acquire Foster Farms for $2b. This follows their cancellation from the CAGNY conference earlier this week

- Banks after the Fed Stress Test assumptions are some of the most severe seen, though better for some of the capital markets sensitive names

- Cleveland-Cliffs and Labrador Iron Ore Royalty as Iron ore rallied in the face of the force majeure declared by Vale on certain contracts

Notes From the Sell Side

The (relief) rally post-market in Snap Inc. shares after the social media firm’s revenue beat is prompting all sorts of rethinks on the Street. Raymond James goes to market perform from underperform as user trends are "stabilizing" with "solid" ad growth. Analyst Aaron Kessler sees the 1Q EBITDA guidance as "likely conservative" and puts the company on track to achieve breakeven EBITDA by 2020. The stock is poised to open nearly 27% higher (putting it near levels last seen in Sept)

On the flip side of earnings related performance, the Netgear spin-off Arlo Technologies got hit with a downgrade from Cowen after its fourth quarter results sent shares down nearly 29%. Cowen analysts led by Jeffrey Osborne are taking a "wait and see" approach now that they’ve downgraded the cloud and security platform to market perform from outperform due to the lower demand levels in the segment. Osborne cited a "significantly" slowing market with the company now "heavily" relying on promotions to reduce inventory.

Cowen is also out with an industry call on the chemical names (recall last week’s results in DWDP, among others). Charles Neivert cuts the outlook on the industry to cautious, while downgrading DWDP, CE, EMN, MEOH and ASIX to market perform. Margin pressures are expected to remain through 2019 with concerns over chemical prices and the macro outlook. The analysts cite low oil prices, slowing GDP, "strained" feedstock supply and logistics.

Tick-by-Tick Guide to Today’s Actionable Events

- Cowen Aerospace/Industrial conference day 1

- 7:00am -- MBA Mortgage applications

- 7:30am -- GM earnings

- 8:00am -- SPOT, BSX earnings call

- 8:30am -- Nov Trade Balance

- 8:30am -- REGN earnings call

- 9:00am -- LLY, APC earnings call

- 9:30am -- SU earnings call

- 10:00am -- GM earnings call

- 4:10pm -- CMG earnings

- 4:30pm -- CMG earnings call

- 7:00pm -- Fed Chair Powell hosts Town Hall with Educators

To contact the reporter on this story: Brad Olesen in New York at bolesen3@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Steven Fromm

©2019 Bloomberg L.P.