‘Celestial Event’ Fades, Like MOMO, not Momo Eyes: Taking Stock

‘Celestial Event’ Fades, Like MOMO, not Momo Eyes: Taking Stock

(Bloomberg) -- I promise you that I’ll keep that viral fad that just won’t go away out of this piece.

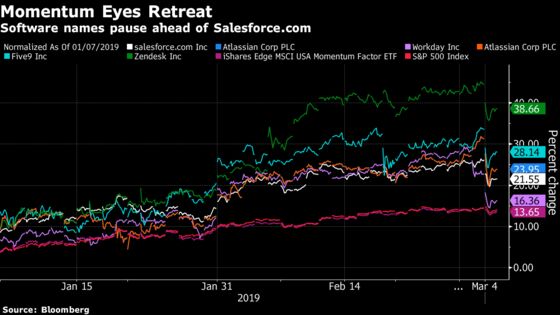

Instead, it’s the focus on how the S&P on Monday provided the perfect opportunity to sell the winners (momentum, or “momo”) into the bullish headlines and strength. After opening above the November highs the index had struggled to exceed for months, it was immediately sold, and the culprits were easy to spot: application software/cloud/productivity names (WDAY, GWRE, ZEN, TEAM, NOW) that had recently hit records ahead of the bellwether in the segment, Salesforce.com’s results.

You may recall going back to Friday this column mentioned that the cloud giant was setting itself up for some seriously high expectations. JPMorgan analysts last week referred to the report as a “celestial event” with "tough" comps for bookings and billings. Goldman Sachs has chimed in post results, calling them "solid", but it was a "high bar" to exceed. Shares dropped more than 3.5 percent through the day, and lost another 3 percent post market as its forecast for the first quarter missed expectations.

And as went the momentum players, so did the market, which happened to close right at its 5-day average figure and not far from the 10-day. Recent bullish trade headlines with China (now further complicated as of this writing, as Trump has now threatened to remove certain favorable trade provisions for Turkey and India) have done little for the S&P 500, implying most of these developments are priced in. Bernstein strategists wrote that some of their macro indicators have suggested a slowing in February, meaning a return to previous highs in the S&P 500 "will take some time." They estimate 2,925 will not come until “late August.”

Snubbed

Two other curious developments on the radar include the action in healthcare, which largely flew under the radar in the shadow of that “celestial” body Monday. Managed care broadly included some of the hardest hit names, as the "Medicare for all" story just won’t go away. You can want it or despise it; but despite the protestations of analysts, who claim there’s no chance of near-term passage, shares continue to fall -- leading me to think someone knows something the rest of the Street does not, or something else is awry.

Retail will also get a shot in the arm today - with results from Target (results just hit the tape with a beat and shares are indicated to open near levels last seen before their 3Q results cratered shares in November, while Kohl’s also just beat and shares are up 4%) and Ross Stores later today. Recall last week’s developments where results from JC Penney and Macy’s and TJX Cos. were all over the map. Target, in addition to results, also has an investor day presentation, which begins at 9am.

Wells Fargo analysts see the struggle for direction in the segment as real. They note investors are trying to determine the driver of some of the weaker results (analysts discussed checks that have shown store traffic through Feb. remains weak) and question whether it’s a “post-holiday lull, unfavorably cold weather, the government shutdown, volatility in tax refunds”?

My Precious

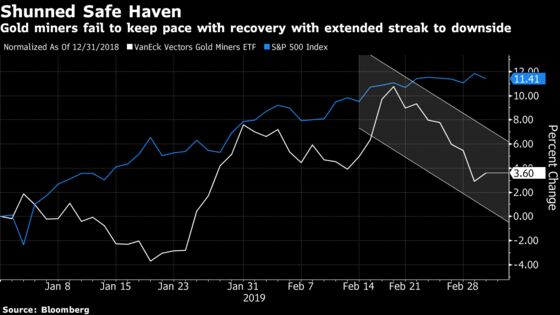

It’s about as fitting a time to talk about gold as ever after the SPX dumped its gains almost immediately on the open Monday, and neared a bit of panic status with the largest selloff in nearly a month before stabilizing in the early afternoon. The so-called safe haven asset has predictably underperformed during this risk-asset boom of 2019, but even in Monday’s action, there was little bid in the commodity, and in fact it extended its downward spiral to the 6th straight day -- the longest downdraft in two years. That streak has now extended to 7 straight days as of writing.

This move infected other gold-impacted areas of the financial markets. As my colleagues Carolina Wilson and Justina Vasquez wrote, the $33 billion SPDR Gold Shares ETF, or GLD, saw the largest net withdrawal in more than a year on Friday, at nearly half a billion dollars. The precious metal dipping below $1,300/oz has long be seen as a key level, and with those declines, pressure will likely build on higher cost miners as their margins may compress. Many larger miners have all-in-sustaining-costs in the $800-900 region. Interestingly, the GDX, Vaneck’s Gold Miners ETF, exhibited mixed performance among the constituents, with nearly half recording gains and half recording losses on the session. Investors also pulled $148 million from that ETF last week as well.

The M&A in the segment also can’t be overlooked, especially in light of the rejected bid Monday in the Newmont/Goldcorp/Barrick saga. Deal talk and financing in the sector was a hot topic at the BMO Metals & Mining Conference, as my colleague Aoyon Ashraf pointed out, and that consolidation is necessary for investors to come back to the segment. The GDX and GDXJ (junior miners) have both underperformed the S&P 500 Materials index this year (~3.8 percent to 8.7 percent).

Sectors in Focus Today

- Cloud and SaaS names (VEEV, ULTI, SAP) after CRM’s results post market failed to galvanize the bulls further; watch other names ZEN, TEAM, NOW and FIVN after they suffered with the overall selling

- Chinese tech ADRs after video streaming services provider HUYA beat expectations (IQ, YY, SINA also reported a beat and is up in the pre-market)

- Managed care names after the relentless selling on "Medicare for all" speculation (CVS, ANTM, UNH, CI)

Notes From the Sell Side

Alnylam’s price target at Morgan Stanley was raised more than 50% to $122 in conjunction with the upgrade that was prompted by David Lebowitz’s expectation that Onpattro sales will exceed the Street estimates in 2019. He also cites the expectation for "positive news flow" emanating from the late stage pipeline for Givosiran and Lumasiran which should drive the share price. Lebowitz discusses metrics that indicate that even with "modest" sequential adds in patients through the year, the company should beat the consensus estimate for sales of Onpattro. Shares are indicated to open higher by nearly 3%.

Lithium miner Sociedad Quimica y Minera de Chile (SQM), following results last week, was cut to neutral from buy at Citi as the analysts are skeptical of the share price performance going forward despite their positive views on long-term lithium demand. Analysts Andrew McCarthy and Juan Tavarez see risks to potential oversupply in 2019 and now would rather wait until fundamentals improve before recommending positions in the company.

Tick-by-Tick Guide to Today’s Actionable Events

- Carnival in Rio

- Optical Networking and Communication Conference in San Diego (AAOI, INFN, JNPR)

- Citi Global Property CEO conference (HHC, RHP, EQR, MAC, DLR, BDN)

- JPMorgan Aviation, transportation and industrials conference (GE, LUV, UAL, AAL, KSU, UNP, R)

- 7:00am -- KSS results

- 8:00am -- CVX analyst meeting

- 9:00am -- TGT, KSS earnings call; TGT, SPXC investor/analyst meetings

- 09:45am -- Feb Markit US Services PMI

- 10:00am -- Feb ISM Non-Manufacturing Index

- 10:00am -- Dec New Home Sales

- 11:30am -- Fed’s Barkin speaks at the Rural Economy

- 1:30pm -- H investor day

- 2:00pm -- Jan Monthly Budget Statement

- 4:00pm -- ROST earnings

- 4:05pm -- URBN results

- 4:15pm -- ROST earnings call

- 7:00pm -- NIO earnings call

To contact the reporter on this story: Brad Olesen in New York at bolesen3@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Steven Fromm

©2019 Bloomberg L.P.