‘Capitulation’ Isn’t a Bad Word for This Rally: Taking Stock

‘Capitulation’ Isn’t a Bad Word for This Rally: Taking Stock

(Bloomberg) -- To the President, that word is profane and anathema to the “Art of the Deal” tenets. An appearance of strength is crucial, but for the bulls, some give is great for the take.

The lift we saw Tuesday after reading between the lines of trade deal optimism was validated when Trump appeared to capitulate on a hard March 1 deadline (could let it slide "for a little while") for tariff and trade negotiations (however, some pointed to reports that the Senate Intelligence committee is purported to have found no collusion with Russians as rationale for some of the rally).

Reports that Chinese President Xi would be joining the trade talks later this week (elevating it from "mid-level" officials) may be bolstering the rally, with futures looking up a couple handles (though off the highs overnight). In an ironic twist for the developer-turned-President, only one sector, real estate, was the source of the only downside after the risk-on rally.

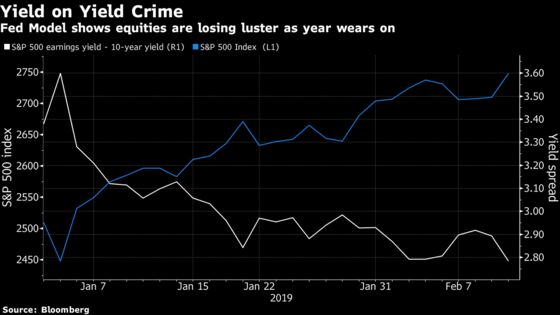

The second-best performing sector of 2019 before Tuesday, real estate suffered at the hands of rising 10-year treasury yields and a steepening of the curve -- a temporary stay of the recessionary fears being voiced by the NY Fed’s favorite recession probability indicator, the spread between three-month and 10-year Treasury yield, according to UBS in a note last week. Using the indicator, odds of a recession hit the highest level since 2008, though the analysts still maintain their baseline projection of growth for the year. A similar concept is displayed in the below chart.

But crucial for that signal will be January CPI figures at 8:30am. Deutsche Bank analysts write that figures will undergo a quality adjustment that may have the effect of lowering the rate, assuming that the inclusion of telecom services.

Up Against It

If inflation remains subdued, we could get a further lift after equities finally pushed through the 200-DMA. The technical level also happens to coincide with valuation risks in the S&P 500 that are attracting more cautious voices each day. Morgan Stanley analyst Mike Wilson has been cautious about the rally for weeks, and Monday slashed his earnings growth prediction (“Earnings recession is here,” he wrote). Bernstein said the same about Europe Tuesday in flagging risks for an earnings recession there. Equities may be "topping out" in the short run, Bloomberg Intelligence Chief Equity Strategist Gina Martin Adams wrote Monday, ahead of the rally we saw Tuesday that added 1.3% to the main gauge. Stocks need a better 2020 earnings outlook to rise much more, she wrote.

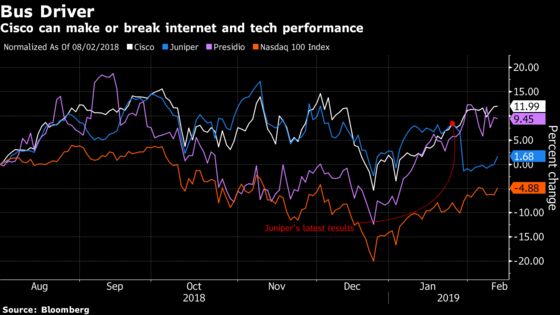

Communication Is Key

And turning to today’s action, I’ve always felt that Sysco and Cisco earnings signal the end of earnings season is nigh (though there remain ~140 more members of the S&P 500 to report), and the latter is upon us with results post-market. Intel, Nvidia, Apple and the other FAANGs have the ability to set the market tone each day. But ignore the $215 billion communications giant that comprises 4.6% of the S5INFT and nearly 3% of the Nasdaq 100 (20% of the Russell 1000 tech value index while we’re on the topic) with a massive supply chain and finger on the pulse of tech at your peril.

Ultimately analysts are bullish (CSCO buys outpace holds by 2:1, according to data compiled by Bloomberg) on results. This, despite communications equipment peer Juniper (though a fraction of CSCO’s size), whose fourth quarter results and forecast two weeks ago sent shares to their worst performance in over 6 months. Results will also play a part in viewing how sentiment in January unfolded given their differing fiscal years.

Keybanc’s Alex Kurtz cites read through in some of the giant’s partners Presidio and ePlus for his optimism, given the two reported better than expected top line results (while we’re on the topic, watch EMKR, AQ (a newish IPO from late 2017 which just saw shares crater 26% pre-market on results), CLS, EGAN and AAOI given they all rely on Cisco for more than 15% of their revenues, according to Bloomberg supply chain data). Raymond James ahead of results also had a positive bias, citing checks that suggest demand from enterprise is still "robust." Analysts there cite valuation, its competitive position and consensus sales growth above their own forecasts as rationale for their outperform rating. Piper Jaffray analysts expect a "solid" second quarter but are "concerned" about third quarter guidance.

Sectors in Focus Today

- Cult consumer names Canada Goose, Yeti ahead of their results Thursday post-market

- Lighting stocks after Bain, Carlyle are said to be considering a bid for Osram (incremental to November reports of interest); watch CREE, AYI, VECO, HUBB

- Content delivery health after AKAM results beat (LLNW etc) and indicate the degree to which its largest customers (MSFT, AAPL, AMZN, NFLX) are utilizing network activity

- Advertisers after IPG reports (OMC lifted the segment, including WPP on Tuesday after Publicis disappointed last week)

- Generic drugs and pharma after giant Teva missed expectations, falling 8.5% pre-market

- Hotels after Hilton results (shares are up 3%), which may give insight into the Govt shutdown issues and spending

- SaaS names after HUBS (+78% in past 12 months), TWLO (+350%), CSOD (+56%) disappointed with relatively muted results after outpacing the market for the better part of a year; all three are indicated to open lower

Notes From the Sell Side

Deere is lower pre-market after BofAML analysts cut their rating to neutral from buy after the risk/reward moves toward more balance after its outperformance ahead of results Friday. Analyst Ross Gilardi is skeptical the industrial bellwether will raise guidance given the global trade environment and softer construction demand. Notes that for it to sustain a premium to Caterpillar, it needs to beat and raise with its results. The soybean tariffs are also seen as a flashpoint for the stock.

Qiwi ADRs were also downgraded this morning, but by JPMorgan analysts, sending shares lower by 2%. Alexei Gogolev calls for taking profits due to the execution risk at the company. His rating moves to neutral after shares rose nearly 40% from its trough in October. Gogolev still expects the instant payment company to beat its guidance and consensus when it reports in mid March, but ultimately sees risks related to the company’s noncore investments.

Tick-by-Tick Guide to Today’s Actionable Events

- Today: TCR2 Therapeutics (TCRR), Cibus (CBUS) IPOs expected to price

- Bank of America Merrill Lynch Insurance conference

- Credit Suisse Financial Services forum

- Goldman Sachs Tech and Internet conference

- Stifel transportation and logistics conference

- 7:00am -- MBA Mortgage applications

- 8:00am -- AFL at Bank of America Merrill Lynch Insurance conference

- 8:30am -- Jan Consumer Price Index

- 8:50am -- Fed’s Bostic and Mester speak

- 9:05am -- ZION at Credit Suisse Financial Services forum

- 9:30am -- CERN investor meeting

- 9:45am -- CIT at Credit Suisse Financial Services forum

- 10:00am -- GRPN, HLT earnings call; EXTR investor day; HIG at Bank of America Merrill Lynch Insurance conference

- 10:30am -- EIA crude oil inventory report

- 11:05am -- NAVI at Credit Suisse Financial Services forum

- 11:10am -- ALL at Bank of America Merrill Lynch Insurance conference

- 11:50am -- LRCX at Goldman Sachs Tech and Internet conference

- 12:00pm -- OXY earnings call

- 12:00pm -- Fed’s Harker speaks on the economic outlook

- 12:40pm -- LITE, AVLR at Goldman Sachs Tech and Internet conference

- 2:00pm -- Dec monthly budget statement; SBCF investor day

- 2:40pm -- TXN at Goldman Sachs Tech and Internet conference

- 4:05pm -- CSCO earnings

- 4:15pm -- AIG, MGM earnings

- 4:30pm -- MRO earnings

- 4;30pm -- CSCO earnings call

- 5:00pm -- GG earnings, MGM earnings call; ADBE at Goldman Sachs Tech and Internet conference

- 5:40pm -- PYPL at Goldman Sachs Tech and Internet conference

To contact the reporter on this story: Brad Olesen in New York at bolesen3@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Steven Fromm

©2019 Bloomberg L.P.