An $8.7 Billion Burden Casts Doubt Over BC Partners Newest Fund

`Amazing Svider Man' Fights to Prove BC Partners Revamp Pays Off

(Bloomberg) -- In late 2017, Raymond Svider was looking back on a bruising year. BC Partners, the pioneering European private equity firm where he had risen to chairman over 25 years, had struggled to hit its fundraising target, some of its high-profile holdings were in trouble, and investors were frustrated at the company’s investment strategy.

Svider gathered his senior partners in London and New York on a conference call and presented them with a plan to overhaul the firm: downgrade their titles from managing partner to partner and promote him from co-chairman to sole head. Svider said the moves would remove bottlenecks and make the company more nimble, and both ultimately passed unanimously.

More than a year later, the French-native, who the New York Post dubbed the “Amazing Svider man” in 2015 after he was reported to spend $32 million on a Park Avenue penthouse, is under pressure from some investors and people inside the firm to prove that his reboot will pay off. BC will start pitching its 11th fund in coming months, aiming to raise cash early next year, people familiar with the matter said.

Svider said he’s excited about the management changes, which will make the firm more nimble, and the perception that the company hadn’t evolved enough with the times is changing. A BC spokeswoman declined to comment on the firm’s fundraising plans, but said that Svider is “universally regarded by our investors as one of our best deal makers, with a proven and long track record of making money for LPs.”

As he prepares to raise the firm’s 11th fund, Svider can ill afford another experience like the last round. It took BC about 18 months before it finally hit its 7 billion-euro ($7.9 billion) target in 2018, losing ground to some competitors. Six months earlier, CVC Capital Partners had raised more than twice that amount in a third of the time, a person familiar with the matter said. Apollo Global Management raised about $24.7 billion in 2017, the largest pool raised by a leveraged buyout fund so far.

“The mood music around BC is that the jury is still out,” said Charlie Bott, BC’s former head of investor relations, who retired in 2018 and still has some interests in the firm’s funds. “The firm is not perfect, but is in a good position with the performance of some of its investments.”

At least one fellow private equity firm agrees with the positives. A unit of Blackstone Group LP that buys stakes in alternative asset managers is considering making a minority investment in BC Partners, people familiar with the matter said Wednesday.

The problem last time was that investors were looking at the performance of BC’s last fully invested fund to gauge returns, and that pool’s largest investment was Intelsat SA. In the months before Svider began raising money for the 10th fund, the European satellite operator’s shares had sunk as much as 92 percent from its initial public offering.

This round, BC’s investment in troubled retailer PetSmart Inc. is making some hesitant to put in more capital, one of BC’s longtime investors said, asking not to be identified discussing private matters. There are also concerns from investors and employees that Svider has given himself too much to do as sole chairman, people familiar with the matter said.

"We did hit our fund target -- it’s true that it took longer than we’d planned but we did make that figure,” Svider said in an interview in New York in October. “What matters is that we got there and we are investing the fund.”

A spokeswoman for BC said that the eighth fund, the pool which included Intelsat, was hit by the last financial crisis and that virtually all private equity firms’ funds raised around the 2005-to-2006 period were disappointing. No one investment affected results and returns were marked at about two-times cost as of September 2018 after a rebound, she said.

Yellow Pages, Springs

BC was founded in 1986 by Otto van der Wyck and John Burgess and was seen as a pioneer in European leveraged buyouts, raising some of the biggest funds on the continent. In an interview in 1999, Burgess talked about the no-frills businesses that appealed most to him -- French hotel linens, the publisher of the Italian yellow pages, a steel spring maker -- at a time when the rest of the world was going mad for dot coms. He said his strategy generated returns “well in excess” of 20 percent a year.

Svider, 56, has been with the firm for most of its history, joining in 1992 and doing stints in Paris and London before moving to New York in 2008. He now runs BC with his executive committee -- partners Nikos Stathopoulos and Jean-Baptiste Wautier and Chief Operating Officer Graeme Dell. Power is spread further with important decisions, such as pay, being made by a separate committee.

Rearview Mirror

The flip side of BC’s historic conservatism is that it’s arguably missed out on returns. One investor hesitated to put money in the last round because he was frustrated at BC’s low appetite for risk, which had protected profit during the last financial crisis but caused it to miss out on a boom in technology stocks. This person, who ultimately contributed to the fund, asked not to be identified because he still invests with BC.

"We were perceived as not having adapted enough to the changed environment, and in my view that was probably right, and now that perception has changed,” Svider said. “You know when you look at something, the image is always what’s in your rearview mirror. That’s human nature.”

Svider also accepted the challenges that Intelsat caused. He championed the $5 billion investment with Silver Lake Partners in 2008, and in the years following the deal, Intelsat’s revenue growth slowed and sales ultimately began to shrink, according to data compiled by Bloomberg. The stock, which BC still holds, has now rebounded to above $20 a share compared to its $18 IPO price.

Fund Nine

As BC considers raising its 11th fund, investors will be looking at the performance of the ninth, its last fully invested pool. The company has invested most of its 10th fund, which is why it’s considering raising more money next year, though it hasn’t sold any of the holdings yet, people familiar with the matter said.

While BC has seen recent strong exits -- including the sell down of its stake in Com Hem Holding AB at a 90 percent premium to the IPO price and the sale of its shares in Sabre Insurance returning three times its investment –- PetSmart isn’t a top performer and the uncertainty around whether the firm’s problems can be fixed have made some of BC’s investors nervous about putting money in another fund, the people said, asking not to be identified discussing a private matter.

BC agreed to buy PetSmart in 2014 as part of a consortium for about $8.7 billion. Svider was the driving force behind the holding where he even stepped in to run the company after its chief executive officer resigned.

"If after fund eight, fund nine also turns out not to be top quartile or even above median, then it will be tricky to raise fund 11," said Ludovic Phalippou, professor of financial economics at Oxford University’s Saïd Business School.

Problem Child

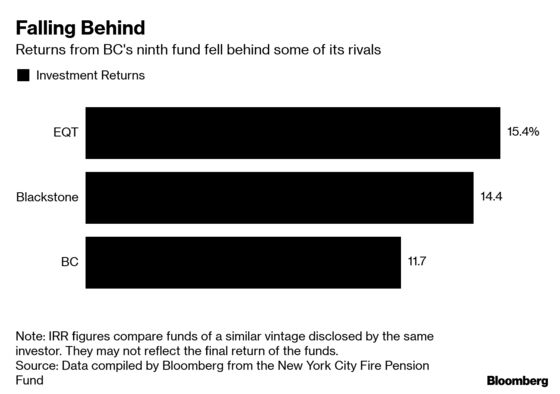

BC’s ninth fund is reporting a 11.7 percent return on investment as of the end of June, according to data disclosed from one of its investors, the New York City Fire Pension Fund. It disclosed that a Blackstone fund raised in a similar year had returned 14.4 percent and EQT’s returned 15.4 percent. BC’s returns were in the bottom half compared to others that started raising money around the same time, according to data compiled by Bloomberg from investors that disclosed the figures.

The private equity firms declined to comment on their funds’ returns.

Numbers from individual investors may not accurately reflect final returns, something that isn’t disclosed publicly, because some investments are active and their values are still changing. But it’s a good measure of BC’s performance relative to peers. A person familiar with BC’s fund said its return is currently 14 percent.

“Every firm has problem children, not every single fund will be top quartile. You have to look at the way they go about business,” said Pierre-Alain Wavre, chief investment officer of wealth management firm Banque Pictet, which has invested in several of BC’s funds. “They consistently have generated strong returns.”

Dog’s Dinner

Wavre says PetSmart is currently marked at about 1.8-times its initial investment. The asset also paid out a $800 million dividend in 2016, people familiar with the situation said at the time.

After BC bought PetSmart, it added online pet food shop Chewy for $3 billion in 2017, a purchase that injected growth even as retail traffic flatlined. The deal also loaded the company with debt, which reached $8.6 billion as of Feb. 3, people with knowledge of the matter said.

Chewy filed plans for an IPO on Monday. The company said that its net sales grew to $3.5 billion last year from $26 million in 2012.

The holding is in the middle of its investment phase, and BC can’t speculate on the outcome, a spokeswoman for the firm said. The investment is marked at above cost in the firm’s accounts, she said.

Svider’s willingness to step in and run PetSmart shows “his accountability, ability and willingness to take charge to improve the performance of an investment that is suffering,” she said.

Next Judgment

BC said that ultimately, the guiding principles behind Svider’s revamp were to make the firm more effective, agile and accountable and points doubters to a string of lucrative deals he’s lead in his more-than quarter century at the firm.

“I’m incredibly excited about the partner changes and have been pushing this for some time,” Svider said in the interview. “Before we had managing partner and senior partner and if we were a law firm both would be called equity partners, except some had more of a management responsibility.”

The firm’s investment in the combined Suddenlink Communications and Cablevision Systems Corp. businesses, its biggest, is lined up to return more than three times its cost while German cable provider Unitymedia, sold in 2010, made the firm a 3.6-times return, the company said. An investment in Office Depot increased in value by 70 percent before it was divested in 2013, while MultiPlan, sold in 2014, doubled their money.

Acuris, a financial data provider that competes with Bloomberg acquired in 2014, also looks likely to deliver a profit once it’s sold. BC acquired Acuris for 382 million pounds ($499 million) from Pearson Plc and is hoping to sell the business for more than 1 billion pounds, people familiar with the matter said in January.

For Svider and BC Partners, the 11th fund will give them an opportunity to put any lingering doubts to rest. "The next judgment will come when we raise again,” he said.

--With assistance from Katherine Doherty.

To contact the reporters on this story: Sarah Syed in London at ssyed35@bloomberg.net;Kiel Porter in Chicago at kporter17@bloomberg.net

To contact the editors responsible for this story: Dinesh Nair at dnair5@bloomberg.net, Amy Thomson, Aaron Kirchfeld

©2019 Bloomberg L.P.