Investors Pull $30 Billion, Just From One Company: Taking Stock

Investors Pull $30 Billion, Just From One Company: Taking Stock

(Bloomberg) -- A few positives across the landscape early this morning, with much of the optimism being attributed to what appears to be a bipartisan agreement in the U.S. Congress to fund elements of border security for both sides of the political spectrum (a smaller barrier than Trump wanted, but a barrier nevertheless, and a rejection of limits Democrats wanted on detentions) -- but more importantly and relevant to equity investors, optimistic lip service from President Trump on making a deal with China.

Some key tech and chip names exposed to the Asia supply chain that have suffered at the hands of the unknown in trade (AMD, MU, XLNX, LRCX, NVDA) are getting a bit of a lift this morning, together with S&P futures, up nearly 19 handles in what is one of the strongest starts we’ve seen from a market that has appeared pensive and noncommittal for the past few weeks.

The optimistic remarks from the Trump administration lack detail thus far, and its unclear whether it changes the prospect of a meeting Chinese President Xi before the March 1 deadline (an issue that soured the mood last week). However, the market may be suspecting that the threat to more than double the rate of tariffs on $200 billion in Chinese imports may be softened.

Also helping sentiment this morning is positive signals from Europe on the health of the luxury consumer. The segment received another shot in the arm after Gucci parent Kering’s results confirmed what we’ve seen from Hermes, L’Oreal and Ralph Lauren on luxury. The CFO said demand from clients in China remained “extremely dynamic” in the fourth quarter. U.S. listed Capri holdings (parent of luxury brands Versace, Michael Kors and Jimmy Choo) is indicated higher in the pre-market. The next consumer bellwether for the U.S. includes results from Under Armour, which has been volatile in the pre-market after fourth quarter earnings and revenue beat expectations but the athletic giant reaffirmed its 2019 outlook. See our preview here.

Legend...Wait for it...dary

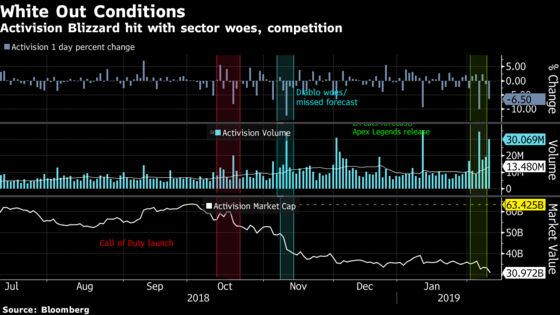

While all of the above macro conditions have been in play, the video game story line has thickened. From what appears to be a brilliant communication strategy employed at Electronic Arts (cutting forecasts with results and within 48 hours touting a massive new surprise hit in Apex Legends --a free-to-play Fortnite competitor that Piper analysts said is on a "blistering" pace for player count), to the now $30 billion loss in market value at Activision Blizzard -- in just four months. Competition is taking a toll, and while EA may have timed its releases and financial results to offset the market’s reaction to the Fortnite craze, Activision was not so lucky.

Combine EA’s difficult non-Apex related sales (that dragged the video game segment lower) with new Bloomberg reports that Activision was said to be cutting hundreds of jobs, and its a death by a thousand cuts. Activision has its work cut out, as Benchmark analysts Monday lowered their price target, citing "cautious" near term expectations and fewer product catalysts for the shares, which fell an additional 7.6% to levels not seen in two years. Shares have fallen in 5 of their last 6 earnings reports, and options are pricing in a nearly 11% move around earnings.

Though EA added to its gains Monday, it curiously erased the gains into the close ahead of Activision’s results today post-market. EA however is still controlling the narrative (do we call it a "cheat code" at this point?) -- in a post-market announcement, they chose to disclose even more players had joined the Apex community (watch shares of Tencent Holdings, which runs the Fortnite franchise). Bloomberg Intelligence analyst Matthew Kanterman, in a note Monday wrote that the "strong momentum" for EA is sustainable, with user growth more important than sales. Shares rose 6.8% and are poised to open at levels seen before their release of the Battlefield V game.

Sectors in Focus Today

- Managed care names (CNC, HUM, UNH) as Molina Healthcare beat expectations; shares rose 6% post market

- Sports apparel and retail as Under Armour earnings beat expectations but reaffirmed; watch FL, DKS, Macy’s and Kohl’s

- Railroads after Norfolk Southern lifted selected peers like Union Pacific in hits forecast for revenue growth Monday

- Software-as-a-Service names ahead of a series of earnings reports for TWLO, LOGM, HUBS, among others (Piper for one said its checks ahead of CSOD’s results post-market are likely to show outperformance, particularly in Europe, and for HUBS they saw "another strong quarter")

- Semiconductor manufacturing after AMKR results disappointed; though its much smaller than other peers like Applied Materials that report Thursday; peers MKSI, KLAC, AMAT, ENTG all reported recently

- Chemical names after Huntsman’s earnings missed expectations; follows poor results from DWDP and EMN earlier this month

- Rent-to-own player RCII and its competitor AAN as the court case involving Vintage capital may wrap today

Notes From the Sell Side

Cisco is indicated lower after the networking giant was downgraded at Morgan Stanley ahead of its quarterly results Wednesday. As the stock approached the analysts’ $51 price target (prev. close $47.58), James Faucette wrote that the pace of prospects in the security segment is "unlikely" to counter the slowing in traditional hardware. He lowered the PT to $49 and the rating to equal-weight from over-weight , citing their survey that found a slowing pipeline for Security sales among resellers.

Varonis had a series of downgrades after the the security software developer’s first quarter and full year forecasts missed estimates. Stifel analysts cut the rating to hold, citing the company’s disclosure to shift to a subscription-based model from perpetual license, a strategy that "meaningfully hampered" the outlook. PT goes to $52 (prev close $63.96), with the stock indicated to open lower by nearly 22%. The subscription model will act as a headwind as ASPs tend to contract when shifting from perpetual licenses and the pace of that shift will be difficult to forecast, they write. JMP also downgraded shares.

Tick-by-Tick Guide to Today’s Actionable Events

- Today --Virgin Trains USA (VTUS) IPO expected to price

- OPEC monthly oil market report published

- Credit Suisse Energy Summit

- Credit Suisse Financial Services forum

- Goldman Sachs Tech and Internet conference

- Stifel Transportation and Logistics conference

- 8:00am -- GS at Credit Suisse Financial Services forum

- 8:30am -- MOH, UAA, SHOP earnings call

- 8:40am -- WFC at Credit Suisse Financial Services forum

- 9:20am -- C at Credit Suisse Financial Services forum

- 9:30am -- HES at Credit Suisse Energy Summit

- 10:00am -- Dec. JOLTS Job Openings;

- 10:00am -- DFS, BLK at Credit Suisse Financial Services forum

- 10:05am -- CPE, Baker Hughes at Credit Suisse Energy Summit

- 10:40am -- CNQ at Credit Suisse Energy Summit

- 11:05am -- LSTR at Stifel transportation and logistics conference

- 11:15am -- NE at Credit Suisse Energy Summit, GOOGL at Goldman Sachs Tech and Internet conference

- 12:40pm -- AMD at Goldman Sachs Tech and Internet conference

- 12:45pm -- Fed’s Powell speaks on rural poverty

- 1:00pm -- OLN investor day

- 1:20pm -- SYMC at Goldman Sachs Tech and Internet conference

- 1:25pm -- WERN at Stifel transportation and logistics conference

- 1:40pm -- MS at Credit Suisse Financial Services forum

- 2:00pm -- MSFT, MU at Goldman Sachs Tech and Internet conference

- 2:20pm -- NDAQ, COF at Credit Suisse Financial Services forum

- 3:00pm -- EVR at Credit Suisse Financial Services forum

- 4:05pm -- ATVI earnings

- 4:15pm -- OXY, GRPN earnings

- 4:30pm -- ATVI earnings call

- 6:30pm -- Fed’s Mester speaks on the economy and monetary policy

- 7:30pm -- Fed’s George speaks on the economy

To contact the reporter on this story: Brad Olesen in New York at bolesen3@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Steven Fromm

©2019 Bloomberg L.P.