Deutsche Bank’s Long Road Back to Its Old Normal

No financial company has exited the equities business of this scale before.

(Bloomberg Businessweek) -- For decades, Deutsche Bank AG had one predominant aspiration: to compete with Wall Street. In abandoning global stock trading, Germany’s biggest bank is giving up on that ambition. No financial company has exited the equities business of this scale before. As Chief Executive Officer Christian Sewing put it in announcing the company’s restructuring on July 7, Deutsche Bank’s “North Star” will now be closer to its Frankfurt headquarters.

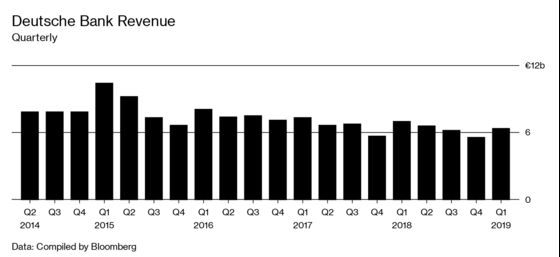

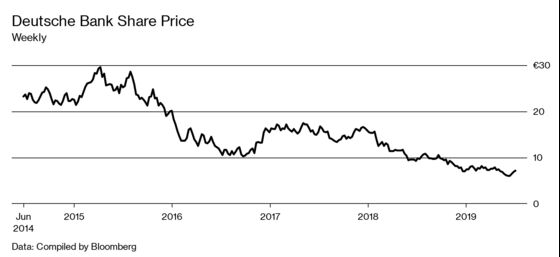

It’s a return to its 150-year-old corporate and trade-finance roots. The sweeping and costly rethink hasn’t come soon enough. Years of mismanagement, multibillion-dollar fines, and declining revenue have eroded the company’s profitability. What was once a powerhouse of global finance has been crippled and left with an uncertain future. Nowhere has the lack of confidence in Deutsche Bank’s ability to survive—let alone thrive—been more visible than in its share price. Down more than 90% from its May 11, 2007, peak to record lows this year, the stock market values the lender at about one-quarter of its physical assets. By comparison, JPMorgan Chase & Co., against which Deutsche Bank vies for business, is eight times more expensive.

Under Sewing, a company lifer who worked his way up from an apprenticeship, Deutsche Bank is finally jettisoning what it was never very good at. The equities business has been losing money for years. In retrenching, the bank will shrink its trading activities by as much as 40%, and about 18,000 jobs—almost 20% of the workforce—will go.

While the loss of jobs will be painful for those involved, eliminating a business that’s been a drag on the company is what Deutsche Bank should have done sooner. Once complete, the pivot will see Deutsche Bank focus more on its corporate customers, large and medium-size companies, at the expense of hedge funds and other financial-services clients.

Over time, the hope is that earnings should be more predictable and evenly spread among lending, trading, asset management, and private banking. The bank should look more like it did when it was founded in 1870 to help finance German industry, but with a sizable fixed-income presence. It will continue to vie for a dominant slice of the world’s debt-financing market, including commercial real estate, the business through which it forged a tie to President Trump. If all goes well, it should become modestly profitable, and from 2022, even be able to buy back shares and pay dividends.

But has Sewing, who’s been in the job since April 2018, bought himself enough time to return to the old normal? Unfortunately, articulating this new strategy has taken the company so long that investors remain incredulous. After an initial rally, shares dropped 5.4% on the first day of trading after the plan was announced. Shareholders will probably want to see Sewing, 49, deliver on his promises before they believe in them. Especially dear to investors is whether the bank will be forced to call upon them to help fund the €7.4 billion ($8.3 billion) reorganization at some point. They’re already missing out on dividends for this year and next.

Sewing’s plan will mark an emblematic shift in the mindset of the organization. A reckless chase for revenue at all costs, a trait that defined its DNA for decades, led to poor profitability and the buildup of risk that’s damaged the bank’s credibility. Sewing was keen to emphasize this break with the past when he presented what he labeled the “reinventing” of Deutsche Bank: Discipline will be key to overcoming a “poor culture of capital allocation,” he said.

Attracted to the growth of its U.K. and U.S. peers in the 1980s and ’90s, the company also jumped on the securities-trading bandwagon. In 1989 it bought London-based Morgan Grenfell. False starts in the U.S. prompted its $9 billion acquisition of Bankers Trust in 1999, a bold deal that created what was then the world’s largest financial-services company.

Among the key engineers of Deutsche Bank’s vision were Swiss banker Josef Ackermann, hired in 1996 to build a global investment bank, and Merrill Lynch fixed-income chief Edson Mitchell, who’d joined a year earlier. By the time of Mitchell’s death in 2000, the securities unit was Deutsche Bank’s most profitable, propelling Ackermann to chief executive officer in 2002. A top recruit of Mitchell’s was former derivatives strategist Anshu Jain, who would go on to succeed Ackermann as co-CEO in 2012. Under Ackermann and Jain, Deutsche Bank became a go-to for risky and complex trades. Backed by an implied state guarantee (some investors even confused it with the central bank because of its name), Deutsche Bank was able to “build up a sheer endless balance sheet,” in the words of one former executive. At its peak in 2007, it had assets of about €2.2 trillion (the figure was closer to €1.3 trillion before the latest revamp).

Although it was able to avoid a government bailout during the financial crisis, Deutsche Bank has never fully recovered. It’s been hobbled by higher regulatory costs and record-low interest rates. It’s also been hit with more than $18 billion of fines, imposed for everything fromlaundering funds for Russians, to rigging interest-rate benchmarks, to misselling mortgage securities in the U.S. The bank’s lax controls have also cost it the trust of regulators in Europe and the U.S.

Rules instated after the financial crisis made the complex transactions the bank had excelled in less profitable, while the core business of trading bonds—the company’s engine during the boom—suffered a permanent contraction. Meantime, in its home market, it’s competing with savings banks and cooperative lenders that aren’t driven by profit margins. The result: Instead of growing, revenue in recent years shrank while costs remained sticky, eroding profitability.

The bank’s Wall Street competitors leapt ahead. U.S. peers significantly bolstered their finances, enabling them to bounce back after the crisis, while Deutsche Bank tried to make do with just tweaking around the edges. The company’s successive reorganizations and leaders failed to address the core of its ills.

But the CEO suite—Jain and co-CEO Jürgen Fitschen were followed by John Cryan in 2015 and Sewing 15 months ago—was only partly to blame for the firm’s procrastination. Those tasked with overseeing the company’s managers, the bank’s supervisory board, exacerbated the problems. In Germany, companies with more than 2,000 employees let workers elect as many as half of their supervisory boards. This created a large and ineffective body that’s been ill-equipped to keep in check the corps of high-flying traders.

In his seven years on the job, Deutsche Bank Chairman Paul Achleitner, a former Goldman Sachs Group Inc. banker who’d advised the company on the Bankers Trust purchase, has advocated for a European investment-banking champion, resisting fundamental change. The company ended up competing across the spectrum of investment banking well after the financial boom had passed. “Too many resources went to businesses where we don’t compete to win and actually leading to underinvestment in areas where we would have far more potential. Simply put, we kept too many options open,” said Sewing, explaining the rationale for the overhaul.

Of late, regulators’ patience with Deutsche Bank has been wearing thin. Officials at the European Central Bank, the lender’s principal supervisor, questioned the logic of a merger with rival Commerzbank AG as the two were holding exploratory talks earlier this year. The combination wouldn’t have addressed the inefficiencies of the investment bank. The companies eventually abandoned the discussions because execution risks, restructuring costs, and capital requirements outweighed the benefits of a merger, the banks said.

ECB officials have suggested Achleitner’s exit would be in the best interest of Deutsche Bank, according to Bloomberg News. The chairman, whose term ends in 2022, has so far retained the support of investors, but it became clear that keeping the investment bank more or less intact was no longer an option. Over the past few weeks, details of the plan began to surface in the media. Investors seemed to like what they heard, pushing the share price up 20% in the 30 days before July 5. With the unveiling of the restructuring on July 7 came the realization that any overhaul at this point will face multiple challenges.

As part of Sewing’s reshaping of Deutsche Bank, the company’s balance sheet should shrink substantially. Noncore assets, mainly trading assets, will be moved to a “bad bank,” a separate unit that will manage and eventually terminate those unwanted holdings. About €280 billion of the so-called leverage exposure associated with these activities should be wound down in three years. That should help to improve the leverage ratio to 5%, from 3.9% at the end of March, and enable the company to return capital to shareholders. While some assets will wind down as contracts expire, others will be sold. That will leave the German bank vulnerable if it fails to get the prices it hopes for them, though management reassured stockholders that its assumptions were conservative.

It’s unclear what effect all these changes may have on, for example, wealth management and investment-banking clients that like to trade across asset classes. Equally, the retreat in rates trading may hurt the remaining transaction-banking operation: Clients may choose to take more of their business away. In short, revenue attrition may be greater than the company expects. It’s far from certain the bank can succeed in increasing revenue at the businesses it intends to keep by about 2% a year through 2022, a key assumption in the path to profitability.

Sewing has overdelivered on savings in his short time at the helm, and his overhaul foresees a further 25% reduction in costs. The bank will be paying less in compensation, but also aims to reduce spending on information technology and consultants. To shield shareholders from paying for the reorganization, Deutsche Bank has agreed with regulators to lower its common equity Tier 1 ratio, its main measure of financial strength.

With capital and revenue expected to get worse before they get better, Sewing doesn’t have much room to maneuver. And what if market conditions worsen? The ECB is expected to cut rates as soon as this summer and more quantitative easing is also on the table. Sewing’s radical reboot is what the company desperately needed. But time isn’t on his side.

To contact the editor responsible for this story: Howard Chua-Eoan at hchuaeoan@bloomberg.net

©2019 Bloomberg L.P.