Markets Finally Start Acknowledging Reality

(Bloomberg Opinion) -- Maybe it’s a case of “buy on the rumor and sell on the news,” but the fact that the MSCI All-Country World Index of stocks was at one point down the most in two weeks on Thursday after news of advances in U.S-China trade talks is a bit concerning.

Besides the dovish turn taken by the Federal Reserve and other major central banks, no other development has contributed more to the rebound in equities this year than optimism that the end of the trade war was in sight. But the action Thursday was less about hope and more about reality — the reality that the global economy is slowing and can no longer be ignored. Activity in Japan’s manufacturing sector contracted in February for the first time in two and a half years, data showed. South Korea, seen as a sort of early warning system for the global economy, said its exports tumbled 12 percent during the first 20 days of the month as shipments of semiconductors plummeted. A report showed German manufacturing shrinking the most in six years. In the U.S., sales of previously owned homes fell in January to the weakest pace since November 2015 despite a big drop in mortgage rates. Yes, that was due in part to the government shutdown, but everybody knew it would get resolved sooner rather than later. “Clearly there’s been a lot weaker data than I think anybody was expecting, including the spate of data that was released today,” Matt Forester, the chief investment officer at BNY Mellon’s Lockwood Advisors, told Bloomberg News.

In short, a trade deal between the two largest economies may be coming too late to reverse the slowdown and the resultant hit to corporate profits. If that’s the case, then investors will need to start recalibrating their portfolios toward an environment that is based more on reality than on hopes. “We’re due to take a break,” Matthew Miskin, a market strategist at John Hancock Investments, told Bloomberg News. “We’ve seen such a huge momentum shift to start the year.”

THIS IS AN EFFICIENT MARKET?

To be sure, markets don’t always act rationally. In fact, a slump in earnings doesn’t always portend bad times for equities. Bloomberg Intelligence’s equity strategists crunched the numbers and found that since the 1950s, U.S. stocks have averaged double-digit gains in calendar years where earnings growth troughed and are up 85 percent of the time. “If the earnings slump is short and doesn’t morph into recession, shares should remain supported,” BI’s Gina Martin Adams and Michael Casper wrote in a research note Thursday. They found that there have been 14 earnings cycles since the early 1950s, with peak-to-trough earnings declines that averaged minus 18.4 percent, or down 8.4 percent without a recession. The average calendar-year price return for these trough years is 11.4 percent. The S&P 500 Index is up 10.8 percent this year, suggesting that it’s possible that stocks do nothing in the rest of 2019 as earnings growth flattens. Current consensus forecasts imply an 11.4 percent decline in earnings per share, from the peak of $42.90 in the third quarter of 2018 to $38 in the current quarter, the BI strategists note. If all this seems a bit odd, it makes sense when you consider that equity traders are eternal optimists, paying now for future performance when earnings do rebound rather than looking in the past.

CHINA EXTENDS A WHEAT BRANCH

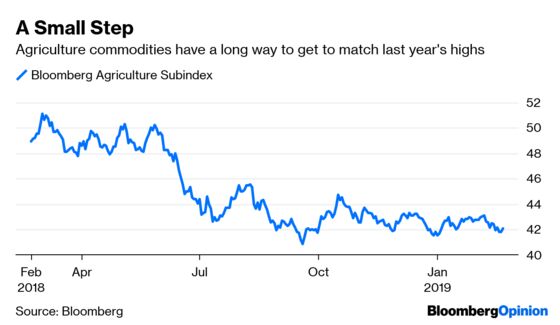

As part of any trade deal, China is proposing that it could buy an additional $30 billion a year of U.S. agricultural products including soybeans, corn and wheat, Bloomberg News reported, citing people with knowledge of the plan, who asked not to be identified because the plans are confidential. The Bloomberg Agriculture Subindex of such commodities promptly jumped as much as 1.21 percent in its biggest gain since November. That sounds impressive, but the index is still down almost 18 percent from last year’s high in March. Any deal may come too late to help struggling farmers. The U.S. Department of Agriculture predicted last week that soybean exports would stay below their pre-trade-war levels until the 2026-2027 season. That followed a report that sales of the oilseed in early January had the worst week ever, according to Bloomberg News’s Millie Munshi and Shruti Date Singh. On top of that, the Federal Reserve Bank of Kansas City warned that farm incomes would likely have a weak start in 2019 and that lenders were tightening credit. In 2017, China imported $24.2 billion in American agricultural products, with 60 percent of that in oilseeds and the remaining in products such as meat, cotton, cereals and seafood. Combined purchases slumped by a third to about $16 billion last year as China’s retaliatory tariffs on American farm goods reduced imports, allowing producers from places such as Brazil, Russia and Canada to fill the void and gain share that they would be reluctant to concede.

WE HAVE A WINNER

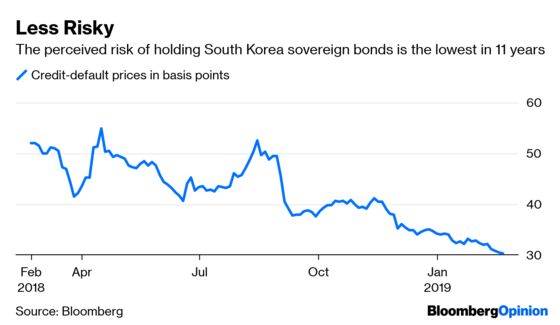

President Donald Trump will meet with North Korean leader Kim Jong Un next week in Hanoi. And while it remains to be seen whether this summit will turn out to be little more than a PR event, one clear market winner has emerged. South Korea’s perceived sovereign bond risk has fallen to an 11-year low amid speculation Trump and Kim may make progress on the denuclearization of the Korean Peninsula, according to Bloomberg News’s Kyungji Cho. Credit-default swaps covering South Korean sovereign notes fell to 30.7 basis points this week, the lowest since November 2007, according to CMA data. Although Moody’s Investors Service would consider boosting Korea’s sovereign rating “if there was a material and irreversible reduction in geopolitical risk,” the path toward denuclearization “remains fraught with uncertainties,” said analyst Christian de Guzman. “An agreement that sees North Korea accede to demands for nuclear disarmament can only contribute to a lasting peace if such commitments are verifiably met and sustained over a longer period of time,” he told Bloomberg News. An adviser to South Korean President Moon Jae-in said Kim was ready to accept the dismantlement and inspection of a high-profile nuclear plant. It’s not just bond investors who are enthusiastic. Global funds bought a net $389.8 million of South Korean stocks on Wednesday, the most since Jan. 25, according to exchange data.

THE U.S. IS RIGHT ABOUT THE YUAN

There was a collective groan from the foreign-exchange community when news broke earlier this week that the U.S. was asking China to keep the value of the currency stable as part of the trade negotiations. The irony is that the U.S. was basically asking China to manipulate its currency to keep it from weakening further and giving its exports a competitive edge after the U.S. has repeatedly threatened in recent years to officially declare China a currency manipulator. But the U.S. might be on to something. China oversaw a 10 percent depreciation in the yuan between April and the end of October, and the Institute of International Finance now estimates in a report Thursday that the yuan is among the most undervalued currencies in emerging markets and needs to rise based on current account imbalances. That runs counter to the consensus, which is that based on the deceleration in China’s economy the yuan should be much weaker and China did global markets a favor by not letting it depreciate faster. China’s current account surplus, which is the broadest measure of trade because it includes investment, has been deteriorating rapidly and may vanish as soon as next year, according to data compiled by Bloomberg.

TEA LEAVES

Canada’s been bucking the trend lately. While major economies have been reporting data that on average have fallen below estimates, Canada’s data have topped forecasts this year, according to the Citigroup Economic Surprise indexes. That’s why it probably doesn’t pay to bet that data due out Friday showing retail sales in Canada slipped 0.3 percent in December from the prior month will be even worse. “While a weak December retail sales print in the U.S. after a strong November presents some downside risks to this release — partially on seasonality effects around Black Friday — November retail volumes in Canada actually did not see any boost,” the strategists at RBC Capital Markets wrote in a research note. Even so, Bank of Canada Governor Stephen Poloz said the path toward higher interest rates is “highly uncertain” because of lingering questions around housing and investment, even as he stuck to his message that borrowing costs eventually need to head higher. Poloz defended the central bank’s five rate increases since mid-2017 and cited two reasons for why he’s been on hold since October last year: the impact of higher rates on indebted consumers and risks to the investment outlook.

DON’T MISS

Modern Monetary Theory Isn’t a Recipe for Doom: Stephanie Kelton

Wall Street Finds That Giving Stuff Away Is Dull: Barry Ritholtz

Europe’s Junk Bonds Are Heading for an Accident: Marcus Ashworth

U.S. Is Rich But With Symptoms of Developing Nation: Noah Smith

Matt Levine’s Money Stuff: Deutsche Bank Lost Money Sometime

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2019 Bloomberg L.P.